Dixon Technologies and Vivo Form Joint Venture for Device Manufacturing

Dixon Technologies has announced a strategic joint venture (JV) with smartphone manufacturer Vivo to produce electronic devices in India. As part of the agreement, Dixon will hold a majority stake of 51% in the JV, while Vivo will own the remaining 49%. This partnership aligns with the Indian government’s “Make in India” initiative and reflects Dixon’s growing role as a key player in the electronics manufacturing ecosystem. The collaboration is expected to strengthen Vivo’s local production capabilities and reduce reliance on imports, while bolstering Dixon’s portfolio in the consumer electronics segment.

Reliance Industries Acquires 74% Stake in Navi Mumbai IIA for ₹1,628 Crore

Reliance Industries Limited has acquired a 74% stake in Navi Mumbai Integrated Industrial Area (IIA) for ₹1,628.03 crore. Navi Mumbai IIA is involved in developing Integrated Industrial Areas (IIAs) in Maharashtra, providing a mix of industrial, commercial, and residential spaces to boost economic activity. The remaining 26% stake in the venture continues to be held by CIDCO (City and Industrial Development Corporation of Maharashtra). This acquisition marks Reliance’s expansion into infrastructure and industrial development, furthering its diversification strategy and strengthening its foothold in Maharashtra’s industrial growth initiatives.

Waaree Energies Secures Solar Module Supply Orders Worth 398 MW

Waaree Energies has received two significant projects from domestic entities for the supply of solar modules with a total capacity of 398 MW. These modules are scheduled for delivery in the fiscal year 2026, underlining the company’s robust order book and leadership in the renewable energy sector. The projects highlight the growing demand for domestically manufactured solar solutions, driven by India’s push for renewable energy self-reliance and sustainability goals.

JSW Energy Bags Renewable Energy Projects Worth 445 MW

JSW Energy has secured multiple renewable energy projects with a combined capacity of 445 MW from commercial and industrial markets. These orders add to the company’s expanding renewable portfolio, pushing its total installed capacity to over 20 GW. This achievement is part of JSW Energy’s commitment to transitioning towards clean energy and aligning with India’s ambitious renewable energy targets. The projects also reflect growing demand for green energy solutions among commercial and industrial clients seeking to lower their carbon footprint.

Summary

These developments showcase a clear trend of Indian companies actively expanding their capabilities across diverse sectors:

Electronics Manufacturing: Dixon Technologies and Vivo’s JV will enhance local manufacturing and strengthen India’s position in the global electronics supply chain.

Infrastructure Development: Reliance’s acquisition of Navi Mumbai IIA positions it as a key player in industrial and infrastructure growth in Maharashtra.

Renewable Energy Focus: Both Waaree Energies and JSW Energy are driving India’s renewable energy agenda, with significant capacity additions and project wins indicating strong market demand for sustainable solutions.

These strategic moves underline the continued momentum in India’s industrial, technological, and green energy growth stories.

Stove Kraft Limited, headquartered in Bangalore, is a leading player in the Indian kitchen appliances market. The company designs, manufactures, and distributes a wide range of kitchen solutions, including pressure cookers, non-stick cookware, gas stoves, mixer grinders, and other small appliances. With strong brands like Pigeon, Gilma, and Black Decker, Stove Kraft has established a significant market presence, catering to both the premium and value-conscious consumer segments.

The company operates through a pan-India distribution network of over 45,000 retail outlets and exports to 14 countries, focusing on innovation, quality, and affordability to drive growth in domestic and international markets.

Key Stock Metrics

Market Capitalization: ₹2,962 crore, reflecting the company’s significant valuation in the kitchen appliances sector.

Current Stock Price: ₹896, trading near its 52-week high.

52-Week High/Low: ₹968 (high) and ₹410 (low), showcasing substantial price appreciation over the past year.

Price-to-Earnings (P/E) Ratio: 86.3, indicating a premium valuation compared to industry peers.

Book Value per Share: ₹138, reflecting the net asset value attributable to each share.

Dividend Yield: 0.28%, offering modest returns to investors through dividends.

Return on Capital Employed (ROCE): 11.3%, indicating efficient use of capital in generating returns.

Return on Equity (ROE): 8.32%, highlighting the profitability relative to shareholder equity.

Face Value: ₹10.0 per share, serving as the nominal value of the stock.

Financial Highlights

Stove Kraft Limited has achieved a remarkable financial transformation, evolving from losses in earlier years to sustained profitability since FY2019. The company’s steady revenue growth, from ₹377 crore in FY2013 to ₹1,420 crore in FY2024 (TTM), reflects strong demand for its kitchen appliances and successful market expansion. Enhanced operational efficiencies have driven an improvement in Operating Profit Margins (OPM) to 10% in FY2024, while net profits have stabilized at ₹34 crore, despite peaking at ₹81 crore in FY2021. The initiation of dividend payouts in FY2023 underscores the company’s financial stability and commitment to shareholder returns. Its balance sheet further highlights robust growth, with equity capital increasing to ₹33 crore and reserves transitioning from negative to ₹423 crore as of September 2024. Investments in fixed assets and capital work in progress (CWIP) demonstrate the company’s focus on scaling operations and infrastructure. While liabilities, particularly borrowings, have risen to ₹1,252 crore, these have been channelled toward productive growth initiatives. Stove Kraft’s ability to maintain this trajectory in a competitive market will depend on continued innovation, efficient capital utilization, and strategic expansion efforts.

Competitive Strengths

Strong Brand Portfolio: Market leadership with well-recognized brands like Pigeon and Black Decker catering to diverse consumer needs.

Wide Distribution Network: Presence in over 45,000 retail outlets ensures extensive reach across urban and rural areas.

Export Growth: Expansion into international markets with a focus on Middle Eastern and South Asian regions.

Product Innovation: Continuous R&D efforts to develop energy-efficient and user-friendly appliances.

Cost-Efficient Manufacturing: In-house production capabilities reduce reliance on third-party suppliers, maintaining competitive pricing.

Risks and Challenges

Raw Material Price Volatility: Dependency on raw materials like aluminium and stainless steel could impact margins.

Intense Competition: Competes with well-established brands like Prestige, Butterfly, and Hawkins in a highly competitive market.

Economic Sensitivity: Changes in consumer spending patterns, particularly in discretionary categories, may affect demand.

Supply Chain Disruptions: Reliance on global supply chains for certain components could pose risks during geopolitical or logistical challenges.

Growth Outlook

Domestic Market: Increased urbanization and rising disposable incomes are expected to drive demand for premium kitchen appliances.

International Expansion: Stove Kraft aims to strengthen its global footprint by entering new markets in Europe and Africa.

Product Diversification: Plans to expand its product portfolio into smart kitchen solutions and energy-efficient appliances.

E-Commerce Growth: Leveraging online platforms to enhance accessibility and cater to tech-savvy consumers.

Recommendation:

Stove Kraft Limited’s stock performance reflects strong market confidence, with its current stock price at ₹892.30, trading close to its 52-week high of ₹950, indicating sustained investor interest. The stock’s 52-week low of ₹750 highlights resilience amidst market fluctuations. With a target price of ₹970 for FY25, analysts project a potential upside driven by the company’s robust financial performance, strategic growth initiatives, and continuous product innovation. Stove Kraft’s focus on expanding its market share in the kitchen appliances sector positions it as a compelling choice for long-term investors, with significant potential for value appreciation as demand in the segment continues to grow.

Paras Defence and Space Technologies Limited (Paras Defence) is a leading Indian company specializing in the design, development, manufacturing, and testing of defense and space engineering products and solutions. Headquartered in Navi Mumbai, the company plays a critical role in supporting India’s defense and space sectors with cutting-edge technologies.

Founded in 2009, Paras Defence operates in highly specialized areas such as optoelectronics, defense electronics, and electromagnetic pulse (EMP) solutions. With a focus on indigenization, the company aligns with the Government of India’s “Make in India” and “Aatmanirbhar Bharat” initiatives. Paras Defence collaborates with global and domestic organizations, making it a key player in India’s strategic sectors.

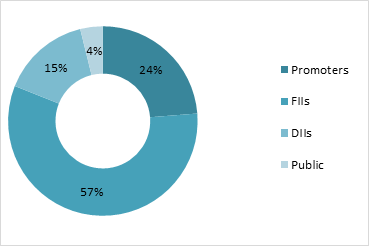

Shareholding Pattern

Business Segments and Products

Paras Defence operates through the following key business segments:

Defense and Space Optics: Offers high-precision optics for satellites, drones, and defense surveillance applications. Supplies lenses and mirrors for electro-optic systems.

Defence Electronics: Specializes in manufacturing rugged electronic systems for defense applications. Provides displays, consoles, and power distribution units for naval and land defense.

Electromagnetic Pulse (EMP) Solutions: Designs EMP protection systems for critical defense and infrastructure installations. Ensures operational continuity during electromagnetic attacks.

Heavy Engineering: Engages in the manufacturing of high-complexity components for defense and aerospace systems.

Additive Manufacturing and 3D Printing: Supports rapid prototyping for defense and aerospace applications using advanced 3D printing technologies.

Financial Performance

Paras Defence has demonstrated consistent growth, driven by its specialization in niche markets. Key highlights include:

Revenue Growth: Revenue has seen an upward trajectory due to increased defense spending and new contract acquisitions. The company has also expanded its footprint in the global space systems market. Q2 FY25 revenue stood at ₹87.09 crore, reflecting a 42.05% YoY growth. Annual revenue for FY24 reached ₹254 crore, marking a 13.87% YoY increase.

Profitability Metrics: Paras Defence’s EBITDA and net profit margins are reflective of its high-value offerings and operational efficiency. Net profit margins are strong at 13.72% for FY24. The company has shown consistent revenue and profit growth, positioning it for long-term stability.

Market Metrics: The current market capitalization of Paras Defence is ₹4,423 crores, and the company generates approximately ₹7.53 lakhs in revenue per employee, demonstrating strong operational efficiency.

Order Book: The company boasts a robust order book, providing visibility for sustained growth over the next few years.

Technological Capabilities

Paras Defence has established itself as a technology-driven company with strong capabilities in:

Optoelectronics: Expertise in optical components critical for surveillance and reconnaissance.

Indigenous Manufacturing: Pioneering solutions aligned with India’s defense modernization goals.

Advanced Testing Facilities: State-of-the-art facilities for testing components under extreme environmental conditions.

R&D Focus: Significant investment in research and development to maintain technological superiority.

Recent Developments and Market Position

Strategic Partnerships: Collaborations with DRDO (Defence Research and Development Organization), ISRO (Indian Space Research Organization), and other leading entities enhance Paras Defence’s market standing. Partnerships with international firms for technology transfers and co-development projects.

IPO Success (2021): Paras Defence raised funds through a successful IPO, signaling investor confidence in its business model and future prospects.

Global Expansion: Increased export of defense systems and components to international clients.

Government Initiatives: Active beneficiary of policies promoting indigenization of defense production.

Future Outlook

Market Trends: The Indian defense sector is projected to grow significantly, with increased budget allocations and a focus on reducing import dependency. Paras Defence is poised to benefit from these trends.

Growth Drivers: Expansion into newer segments like unmanned aerial systems and space-grade components. Participation in mega-projects like India’s lunar and Mars missions.

Challenges: Competition from global defense giants and stringent regulatory frameworks.

Comparative Analysis

When benchmarked against peers like Bharat Electronics Limited (BEL) and Data Patterns, Paras Defence has carved a unique niche with its focus on EMP solutions and optoelectronics. However, its smaller scale and dependency on government projects could be potential constraints compared to larger players.

Metric

Paras Defence

BEL

Data Patterns

Revenue Growth

Higher in niche

Moderate in broad base

High in electronics

Technological Expertise

Specialized

Diverse

Moderate

Export Contribution

Growing

Established

Emerging

Stock Performance and Target

Recent Performance: The stock is currently trading at ₹1,078 (as of December 2024), with a 52-week high of ₹1,592.7 and a low of ₹610. YTD gain: +52.68%, showcasing strong investor confidence.

Target for FY25: Analysts predict a moderate rise of 0.41% to 1.12% by year-end, with targets between ₹1,102 and ₹1,110. Long-term potential: Analysts remain optimistic about the company’s prospects, supported by robust government defense spending and export growth.

Fund houses and wealth managers are raising concerns about the rising trend of investors purchasing international exchange-traded funds (ETFs) trading at significant premiums to their net asset value (NAV). The caution comes amidst a surge in interest among Indian investors seeking exposure to global markets, particularly the U.S., following Donald Trump’s recent victory in the U.S. Presidential election.

International ETFs, designed to provide investors with access to foreign markets, are seeing a mismatch in demand and supply due to regulatory restrictions on the creation of new units. This imbalance has caused many ETFs, especially those tracking U.S. markets, to trade at premiums well above their NAVs. Experts warn that such buying behaviour could lead to disappointing returns when the premium diminishes, and the ETF’s market price aligns with its underlying NAV.

What Are ETFs, and Why the Premium?

ETFs are passively managed investment instruments that track indices, commodities, or baskets of securities, offering low expense ratios compared to mutual funds. They are traded on exchanges like stocks, allowing investors to enter or exit positions throughout the trading day. Fund houses typically appoint market makers to provide liquidity, and large investors can approach fund houses for unit creation or redemption.

However, a demand-supply mismatch has emerged due to regulatory limitations on fresh unit creation in international ETFs. This has led to existing units being in short supply, driving up their prices on exchanges relative to their NAV.

Industry Experts Weigh In

Prateek Bhardwaj (hypothetical name), an experienced wealth manager, explained the risk: “Investors need to understand that paying a premium over NAV is essentially overpaying for the asset’s intrinsic value. When the market price converges with the NAV, it could result in losses or reduced returns. This is particularly risky for investors eyeing short-term gains.”

Another mutual fund executive noted, “The current premiums are a result of pent-up demand for global diversification, especially in the U.S. market, where optimism has risen post-election. However, without new units being created to meet this demand, the price distortion will persist.”

The Risks of Buying at a Premium

Purchasing ETFs at a premium means that investors are essentially paying more for the same value of underlying assets. Over time, as supply stabilizes or investor interest wanes, the ETF’s market price may decline to align with the NAV. This convergence can erode investor returns, particularly for those who bought during periods of inflated demand.

What Should Investors Do?

Wealth managers and fund houses recommend a cautious approach:

Monitor NAV and Market Price: Investors should ensure that they are not overpaying for ETFs by comparing the market price with the NAV before making a purchase.

Evaluate Long-Term Goals: International ETFs are best suited for long-term diversification. Short-term investments, especially during periods of price premiums, could result in suboptimal returns.

Be Patient: Experts suggest waiting for market corrections or fresh unit creations to stabilize prices, reducing the risk of buying at inflated levels.

Seek Professional Advice: Investors uncertain about their strategies should consult financial advisors to assess the suitability of international ETFs for their portfolios.

Why the Renewed Interest in U.S. ETFs?

The U.S. market has attracted renewed attention from Indian investors due to its robust economic performance, diversification benefits, and perceived growth potential following the recent political changes. ETFs tracking major U.S. indices, such as the S&P 500 or Nasdaq-100, are seen as effective vehicles for accessing these opportunities.

However, experts emphasize that such investments require due diligence. While the demand for global diversification is a positive trend, overpaying for these instruments during times of supply constraints could undermine the very benefits they offer.

Conclusion

International ETFs offer a valuable opportunity for Indian investors to diversify their portfolios and gain exposure to global markets. However, the current scenario of ETFs trading at a premium to NAV calls for restraint. Investors must prioritize research and avoid impulsive decisions driven by market trends. By focusing on long-term strategies and understanding the dynamics of ETF pricing, investors can maximize their returns while minimizing unnecessary risks.

MobiKwik, one of India’s leading digital payment service providers and BNPL (Buy Now Pay Later) platforms, is set to launch its much-anticipated Initial Public Offering (IPO). This IPO marks a significant milestone for the fintech giant as it seeks to expand its operations and strengthen its position in the rapidly growing digital payment ecosystem. The MobiKwik IPO, a much-anticipated book-built issue worth ₹572 crore, comprises a fresh issue of 2.05 crore shares. The subscription period runs from December 11, 2024, to December 13, 2024, with the share allotment expected on December 16, 2024, and the listing date tentatively set for December 18, 2024, on the BSE and NSE. The price band for the IPO is set at ₹265 to ₹279 per share, with a minimum lot size of 53 shares, requiring retail investors to invest at least ₹14,787. For small Non-Institutional Investors (sNII), the minimum investment is 14 lots (742 shares), totalling ₹2,07,018, while big Non-Institutional Investors (bNII) need 68 lots (3,604 shares), amounting to ₹10,05,516.

IPO Subscription Period

The MobiKwik IPO is scheduled to open for subscription on December 11, 2024, and will close on December 13, 2024. The share allotment is expected to be finalized by December 16, 2024, with the tentative listing date set for December 18, 2024, on both the BSE and NSE.

Pricing and Lot Details

The MobiKwik IPO offers investors an opportunity to participate in the growth of one of India’s leading fintech companies. Key details are as follows:

Price Band: ₹ ₹265 to ₹279 per share. The lower end of the price band is ₹265, while the upper cap is ₹279.

Lot Size: Investors must purchase a minimum of 53 shares, amounting to approximately ₹14,787 for retail investors at the upper price band.

Issue Size: The IPO aims to raise ₹572 crore, comprising a fresh issue of 2.05 crore shares.

Face Value: ₹2 per equity share. The face value represents the nominal value, with the IPO price reflecting a premium based on the company’s valuation and market demand.

The MobiKwik IPO follows a structured bidding system designed to cater to various investor categories, including retail investors and high-net-worth individuals (HNIs). Below is a breakdown of investment requirements:

Application

Lots

Shares

Amount (Rs.)

Retail (Min)

1

53

14,787

Retail (Max)

13

689

1,92,231

Small HNI (Min)

14

742

2,07,018

Small HNI (Max)

67

3,551

9,90,729

Large HNI (Min)

68

3,604

10,05,516

Reservation Structure

The MobiKwik IPO has a structured reservation system to ensure participation from various investor categories:

Qualified Institutional Buyers (QIBs): 75% of the total issue is reserved for QIBs. This includes mutual funds, foreign institutional investors, banks, and other large financial institutions.

Non-Institutional Investors (NIIs): 15% of the issue is allocated to NIIs, including high-net-worth individuals (HNIs) who bid for larger lot sizes. Small HNIs (sNIIs): Minimum 14 lots (742 shares). Large HNIs (lNIIs): Minimum 68 lots (3,604 shares).

Retail Investors: 10% of the issue is reserved for retail investors, with a minimum lot size of 53 shares, requiring an investment of ₹14,787 at the upper price band.

Key Dates & Timelines

MobiKwik IPO Timeline (December 2024)

IPO Open Date: Wednesday, December 11, 2024

IPO Close Date: Friday, December 13, 2024

Basis of Allotment: Monday, December 16, 2024

Initiation of Refunds: Tuesday, December 17, 2024

Credit of Shares to Demat Accounts: Tuesday, December 17, 2024

Listing Date on BSE and NSE: Wednesday, December 18, 2024

Book Running Lead Managers

The MobiKwik IPO is being managed by the following Book Running Lead Managers (BRLMs):

SBI Capital Markets Limited

DAM Capital Advisors Limited

The registrar for the IPO is Link Intime India Private Ltd, which is responsible for processing applications and managing the allotment process.

Promoters Information

Here is the promoter and key management information for the Mobikwik Systems Limited IPO:

Bipin Preet Singh: Co-founder, Managing Director, and CEO One Mobikwik Systems Limited. He is a visionary entrepreneur and one of the founding pillars of MobiKwik. With a degree in engineering from the Indian Institute of Technology (IIT) Delhi, Bipin has over two decades of experience in technology and innovation. He conceptualized MobiKwik in 2009 with a vision to create a cashless economy in India. Under his leadership, MobiKwik has emerged as a leading digital payment service provider, catering to over 161 million users and 4.26 million merchants as of June 2024. Bipin continues to steer the company’s strategic direction, focusing on innovation and customer-centric solutions.

Upasana Taku: Co-founder, Chairperson, and COO, Upasana Taku co-founded MobiKwik alongside Bipin Preet Singh. She holds a Master’s degree in Management Science and Engineering from Stanford University. With expertise in payments and financial technology, she has been instrumental in building MobiKwik’s operational frameworks, user acquisition strategies, and business scalability. Upasana is also recognized as one of India’s top women entrepreneurs and has driven key initiatives such as MobiKwik ZIP and other financial products. Her focus remains on enhancing operational efficiency and creating innovative credit products.

Koshur Family Trust: Promoter Entity, his trust is an institutional promoter holding a significant stake in the company. The trust ensures compliance and governance while supporting the long-term growth vision of MobiKwik.

Narinder Singh Family Trust: Promoter Entity, Like the Koshur Family Trust, this entity contributes to the company’s governance structure and provides backing for MobiKwik’s strategic initiatives.

About One Mobikwik Systems Ltd.

One Mobikwik Systems Limited is a leading fintech company founded in March 2008, with a mission to drive financial inclusion for underserved populations in India. The company offers a wide range of digital wallets, payment solutions, and financial services. As of June 30, 2024, Mobikwik boasts 161.03 million registered users and 4.26 million merchants, enabling seamless transactions both online and offline. The Mobikwik app offers users a variety of payment methods, such as UPI, Mobikwik Wallet, and co-branded credit cards. Consumers can pay utility bills, shop at e-commerce platforms, purchase goods at retail outlets, and transfer money. A standout feature, Pocket UPI, allows users to make payments without linking a bank account, offering greater flexibility and ease of use.

Mobikwik has diversified its offerings to include credit products like MobiKwik ZIP, a pay-later service with a 30-day interest-free credit line, and ZIP EMI, which provides installment-based personal loans. Additionally, the platform provides investment products such as mutual funds, digital gold, fixed deposits, and peer-to-peer lending, enhancing its financial services portfolio. Advanced features like Lens, which offers personalized financial insights, further enrich the user experience.For merchants, Mobikwik offers digital payment acceptance tools, including POS devices and soundboxes, helping businesses across Tier 2+ cities, small retailers, and large chains accept payments more efficiently. This fosters financial inclusion and supports the digital economy’s growth by catering to diverse merchant needs.With its platform-based approach, Mobikwik is empowering millions of users and merchants, driving digital payments and financial inclusion in India

MobiKwik’s key strengths include its efficient customer acquisition model, with a low cost of ₹32.87 per user, driving substantial growth in its customer base without significant marketing expenditures. The platform also benefits from high repeat usage, with 90.30% of users returning to its MobiKwik ZIP pay-later service, demonstrating strong consumer trust. Furthermore, MobiKwik has seen robust growth in its wealth management services, evidenced by its ₹18,348M AUM in its Xtra product. The company’s use of AI-driven insights to provide personalized financial guidance enhances the user experience, while its strong brand recognition in digital payments ensures high engagement and steady daily activity. Its scalable technology platform further enables seamless transactions and ensures high system availability, supporting its large user base and operational efficiency.

However, MobiKwik also faces several risks. Regulatory oversight by the RBI could impact its operations, as fintech companies are subject to evolving regulations. Additionally, any changes in how the net proceeds from its IPO are used could affect the company’s ability to meet its revenue expectations. Security breaches remain a significant concern, as such incidents could severely damage its reputation and financial performance. The growth in its financial services segment may not match historical trends, which could limit its ability to scale. Losing key consumer or partner networks poses another risk, potentially affecting its revenue and future prospects. Lastly, intense competition in the fintech industry from larger players like Paytm and PhonePe presents a constant challenge to MobiKwik’s market position.

These strengths and risks collectively shape MobiKwik’s strategic outlook in the competitive fintech market.

Financial Highlights

Particulars

FY24

FY23

FY22

Revenue from Operation (in ₹ million)

8750.03

5394.67

5265.65

Profit/Loss After Tax (PAT) (in ₹ million)

140.79

-838.14

-1281.62

Net Worth (in ₹ million)

1625.89

1426.94

2165.42

Earnings per share in ₹

2.46

-14.66

-23.04

EBITDA (in ₹ million)

372.2

-559.2

-1154.06

Total Borrowings (in ₹ million)

2116.99

1922.73

1509.14

Return on Net Worth (RoNW) (%)

8.66

-58.74

-59.19

IPO Objectives

The objective of MobiKwik’s Initial Public Offering (IPO) is to raise capital to fund its growth and expansion plans. The company intends to use the proceeds to enhance its product offerings, strengthen its technology infrastructure, and invest in customer acquisition to attract more users and merchants. Additionally, a portion of the funds will be utilized to repay or prepay certain borrowings, reducing its debt and improving financial stability. The IPO also aims to support general corporate purposes, including administrative costs and strategic investments. By going public, Mobikwik seeks to enhance its brand visibility, provide liquidity for existing shareholders, and establish access to public markets for future fundraising. These objectives align with the company’s vision of scaling its digital payments and financial services ecosystem in India’s rapidly growing fintech market.

Subscription Status

Investor Category

Subscription (Times)

Retail Individual Investors (RIIs)

134.67

Non-Institutional Investors (NIIs)

108.95

Qualified Institutional Buyers (QIBs)

119.5

Employees

Data not specified

Overall

119.38

Conclusion

Should You Participate in the Mobikwik IPO?

Deciding to invest in Mobikwik’s IPO depends on evaluating the company’s fundamentals, market position, and growth potential relative to risks. Here are key points to consider:

Reasons to Participate

Growth Potential in the Fintech Sector: India’s digital payments market is expanding rapidly, and Mobikwik is well-positioned to benefit from this trend with its strong presence in mobile wallets and Buy Now Pay Later (BNPL) services.

Revenue Growth: The company has shown steady growth in revenue, driven by increased user adoption and merchant partnerships, indicating strong business traction.

Digital Ecosystem Synergy: Mobikwik’s ability to integrate payments, lending, and financial services within a single platform creates cross-selling opportunities and a competitive edge.

Improved Unit Economics: Recent reductions in cash burn and operating expenses signal progress toward profitability.

Reasons to Reconsider

Profitability Concerns: The company has yet to achieve consistent profitability, and its path to sustained positive earnings remains uncertain.

Highly Competitive Market: Mobikwik faces fierce competition from well-funded players like Paytm, PhonePe, and Google Pay, which could impact its market share and margins.

Dependence on BNPL Growth: A significant portion of its future growth relies on BNPL adoption, which is subject to regulatory scrutiny and economic cycles.

Valuation Risks: Concerns about the IPO pricing being on the higher side might reduce the upside potential for investors.

Recommendation

If you have a high-risk appetite and believe in the long-term growth of India’s fintech industry, the Mobikwik IPO could be a strategic addition to your portfolio. However, investors seeking stability and immediate returns may prefer to wait for further clarity on the company’s profitability and competitive positioning. A diversified approach to fintech investments is advisable to mitigate risks.

Sai Life Sciences IPO is a book-built issue. The company will raise around ₹3,042.62 crores via an IPO that comprises a fresh issue of ₹3,042.62 crores and an offer for sale of up to 38,116,934 equity shares with a face value of ₹1 each.

About Sai Life Sciences Limited

Founded in January 1999, Sai Life Science Limited partners with innovative pharmaceutical and biotech companies, offering services in drug discovery, development, and the manufacturing of small-molecule new chemical entities (NCEs). As a leading contract research, development, and manufacturing organization (CRDMO), the company leverages its scientific expertise to address critical healthcare challenges.

Sai Life Science envisions a future where it develops ground-breaking medicines to treat currently incurable conditions, significantly advancing healthcare. Its flexible service offerings cater to diverse client needs, from small start-ups to global pharmaceutical giants, showcasing adaptability and resilience.

The company has outpaced competitors in the CRDMO sector, achieving impressive revenue and EBITDA Compound Annual Growth Rates (CAGR) from FY 2022 to 2024. Over the past 24 years, it has consistently delivered a broad range of NCE development programs. Sai Life Science stands out by excelling in three key areas: quality, competitive pricing, and exceptional responsiveness, creating substantial value for its clients.

IPO Subscription Period

Open Date: December 11, 2024

Close Date: December 13, 2024

Allotment Date: December 16, 2024

Listing Date: December 18, 2024

Stock Exchanges: BSE and NSE

Pricing Details

Price Band: ₹522 – ₹549 per Share

Face Value: ₹1 per Share

Minimum Lot Size: 27 shares

Investment Requirement:

Retail Investors: Minimum ₹14823 (27 shares)

Small Non-Institutional Investors (sNII): 13 lots (351 shares) – ₹207522

Big Non-Institutional Investors (bNII): 68 lots (1836 shares) – ₹1007964

Credit of Shares to Demat: Tuesday, December 17, 2024

Listing Date: Wednesday, December 18, 2024

Cut-off time for UPI mandate confirmation: 5 PM on December 13, 2024

Book Running Lead Managers

Sai Life Sciences Limited has appointed prominent financial institutions as book-running lead managers for the IPO:

Kotak Mahindra Capital Company Limited

Jefferies India Private Limited

Morgan Staley India Company Private Limited

IIFL Securities Limited

Kfin Technologies Limited has been designated as the registrar for the IPO.

Promoter Information

Promoter: The promoters of the company are Kanumuri Ranga Raju, Krishnam Raju Kanumuri, Kanumuri Mytrey, Sai Quest Syn Private Limited, Sunflower Partners, Lily Partners, Marigold Partners and Tulip Partners.

Shareholding:

Pre-Issue: 40.48%

Post-Issue: 35.1%

Financial Highlights

Revenue: In FY22 revenue was ₹897 crores, in FY23 it was ₹1245 and in FY24 it is ₹1494

Profit After Tax (PAT): From FY22 to FY24 PAT has increased by more than 10 times, from ₹ 6.23 crores to ₹82.8 crores

Net Worth: ₹974 crores

Total Borrowing: ₹710 crores

Key Performance Indicators (KPIs):

ROE: 11.79%

RoNW: 8.13%

P/BV: 10.18

EPS (Pre-IPO): ₹4.34

EPS (Post-IPO): ₹2.69

P/E Ratio (Pre-IPO): 126.42x

P/E Ratio (Post-IPO): 203.82x

IPO Objectives

The company propose to utilise the Net Proceeds towards funding the following objects:

Repayment/prepayment in full or part, of all or certain outstanding borrowings availed by the Company and

General corporate purposes

Subscription Status (As of December 12, 2024, 7:02:07 PM)

Retail: 0.43x

QIB: 3.2x

NII: 0.6x

Overall Subscription: 1.26x

Recommendation

Sai Lifesciences, an innovation-driven CRDMO and global healthcare product developer serving 25+ leading pharma companies, has shown steady revenue growth and a sharp rise in profitability for FY24. While the IPO is aggressively priced based on FY25 earnings and offers limited direct benefits to the company, it plans to raise ₹950 crore, with ₹720 crore allocated for debt repayment. Despite high valuations, the company is well-positioned to benefit from industry growth driven by supply chain diversification. We recommend subscribing for long-term to the IPO.

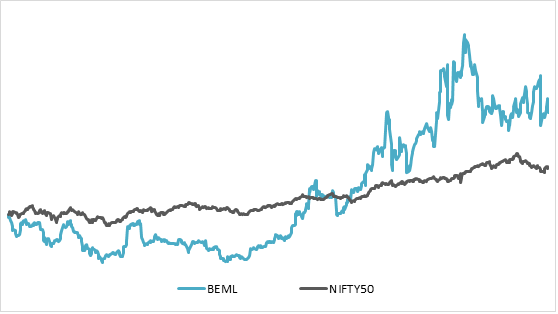

Bharat Earth Movers Ltd. (BEML), headquartered in Bengaluru, India, is a leading public sector undertaking under the Ministry of Defence. Established in 1964, BEML has evolved into a diversified engineering powerhouse, catering to critical sectors including defense, railways, and construction. The company plays a pivotal role in India’s infrastructure and defense development. BEML is a key supplier of military equipment to the Indian armed forces, producing high-mobility vehicles, tank transporters, and missile launchers. BEML offers a comprehensive range of heavy-duty machinery for mining and construction projects, including dump trucks, bulldozers, excavators, and loaders. BEML has a strong domestic footprint and is steadily expanding its international presence, with exports to over 68 countries.

Return Summary

YTD

1 Month

6 Month

1 Year

2 Year

3 Year

5 Year

57.82%

9.05%

10.47%

82.19%

190.46%

129.85%

353.97%

3 Year Return: BEML v/s NIFTY50

Result & Business Highlights

Revenue for YoY and QoQ is at increasing phase at Q2 FY25 revenue of ₹860 crore with a moderate EBITDA margin of 8% at ₹73 crore.

Business segments contribution is Defence & Aerospace 19%, Mining & Construction 43% and Rail & Metro 38%.

BEML exports over 1400+ equipment to 72 countries; railway products are exported to the SAARC region.

Export turnover in FY20 was ₹463 crores, which is now over ₹1066 crores in FY24 and is ₹196 crore in Sep 2024.

Major accomplishment of BEML are 350 armoured vehicles, 3560 military wagons, 2000 metro cars and 18000 rail coaches.

The company has won new contracts worth ₹136 crore and ₹83 crore from the Ministry of Defence.

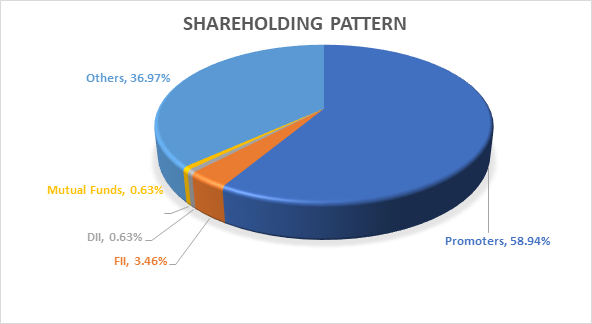

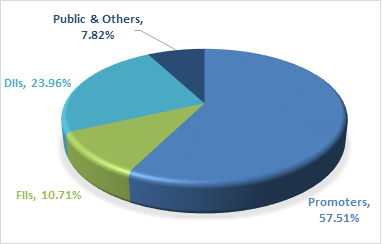

Shareholding Pattern

Return Comparison with Peers

COMPANY

1 Year

2 year

3 Year

5 Year

BEML

82.19%

190.46%

129.85%

353.97%

Hindustan Aeronautics

66.55%

241.84%

612.54%

1123.19%

Bharat Dynamics

78.41%

156.77%

501.51%

750.86%

Paras Defence

58.46%

81.63%

53.49%

–

MTAR Technologies

(23.53%)

3.52%

(27.29%)

–

Contribution to Industry Size

The Indian defence manufacturing sector is valued at approximately $12 billion, with a goal to reach $25 billion by 2025 under the government’s “Make in India” initiative. BEML is a critical supplier of high-mobility vehicles, tank transporters, missile launchers, and ground support equipment. The company supports over 40% of the market for high-mobility military vehicles, positioning it as a key enabler of indigenous defence manufacturing. The Indian mining and construction equipment market is valued at around ₹25,000 crore (~$3 billion), with steady growth driven by infrastructure investments. The Indian railways and metro rail systems are part of a $20 billion industry, with significant investments in urban transit expansion. It holds a dominant position in metro coach manufacturing, supplying vehicles for major cities like Delhi, Bengaluru, and Mumbai.

Balance Sheet Analysis

Reserves are stable at ₹2038 crore from FY21 to ₹2650 crore with high revenues and efficient management operations to ₹4054 crore in FY24.

Borrowing has reduced year on year, makes no worry.

Trade receivables are increasing makes a worry for company in collection of income form government.

Cash Flow Analysis

Cash flow from Operations is ₹560 crores in FY23 and ₹458 crores in FY24.

The Company has purchased fixed assets worth ₹101 crore in FY24, shows a great sign of expansion.

Company is paying dividends continuously every year to its shareholders, shows a positive sign of stable company.

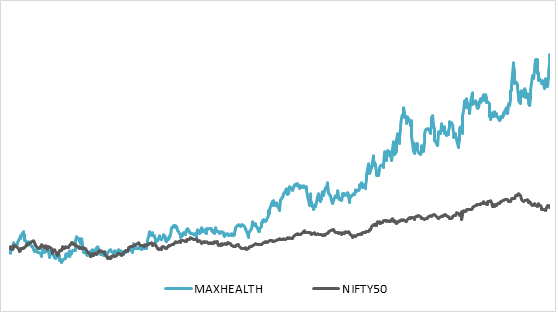

Max Healthcare Institute Ltd. (MHIL) is one of India’s leading providers of healthcare services, known for its comprehensive and integrated approach to healthcare. Established in 2000 and headquartered in New Delhi, MHIL operates a network of hospitals and healthcare facilities that deliver world-class medical services. The company has a significant presence in North India and offers a wide range of services across multiple medical disciplines. MHIL operates 17 healthcare facilities, including tertiary and quaternary care hospitals, primary care clinics, and specialized centers. Its flagship hospitals include Max Super Speciality Hospitals in Saket, Patparganj, and Shalimar Bagh in Delhi-NCR. Max Healthcare aims to continue its leadership in the Indian healthcare sector by expanding its capacity, investing in cutting-edge technology, and enhancing its presence in underserved markets.

Return Summary

YTD

1 Month

6 Month

1 Year

2 Year

3 Year

5 Year

59.84%

5.01%

33.4%

60.59%

150.66%

189.16%

–

3 Year Return: MAXHEALTH v/s NIFTY50

Result & Business Highlights

Revenue for YoY and QoQ is at increasing phase at Q2 FY25 revenue of ₹1707 crore with moderate EBITDA margin of 26% at ₹451 crore.

Average Revenue per Occupied Bed (ARPOB) for Q2 was ₹76,100, with a growth of 7% for existing hospitals.

Newly operational Max Dwarka hospital reported revenue of ₹33 crore, EBITDA loss of ₹18 crore, 41% occupancy, and ARPOB of ₹80,000; expected to break even before year-end.

Acquisition of Jaypee Hospital, Noida, valued at ₹1,660 crore, anticipated to enhance presence in the National Capital Region; plans to increase operational bed capacity from 376 to 430 by March 2025.

Ongoing expansions include 140 beds at Nagpur, 268 beds at Nanavati, 400 beds at Max Smart, 155 beds at Mohali, and 501 beds at Sector 56 Gurgaon, all on schedule.

Max Home reported a revenue of ₹53 crore, a growth of 24% YoY, offering 14 specialized service lines across 12 cities.

Max Lab generated gross revenue of ₹47 crore, reflecting a strong growth of 21% YoY, with over 1,100 collection centers

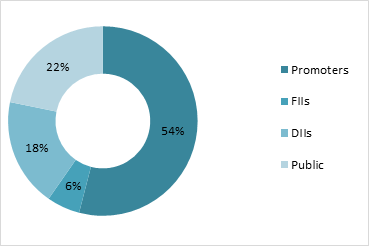

Shareholding Pattern

Return Comparison with Peers

COMPANY

1 Year

2 year

3 Year

5 Year

Max Healthcare

60.59%

150.66%

189.6%

–

Apollo Hospitals

30.37%

52.24%

33.91%

390.48%

Fortis Healthcare

78.88%

141.12%

143.11%

403.41%

Aster DM Healthcare

20.4%

111.31%

151.8%

212.8%

Narayana Hrudayalaya

8.35%

73.5%

129.73%

341.5%

Contribution to Industry Size

Max Healthcare is one of the largest healthcare companies, contributed a lot to its industry and to India. The underpenetration of hospital beds and demand supply gap is reduced and the insurance penetration in healthcare sectors is rising from 32% in FY17 to 41% in FY24. The operations or any surgery procedure cost in India is approximately 70% – 90% discount to average global cost. The increasing use of latest technology in the treatment process has benefited the healthcare industry be efficient and useful in cost cutting also. The occupancy of Max Healthcare is approx. 75%, while others in industry are at average of 65%.

Balance Sheet Analysis

Reserves have increased very significantly from FY21 with high revenues and efficient management operations to ₹7436 crore in FY24.

Borrowing has increased year on year but in significant manner, makes no worry.

The cash on balance sheet is enough to pay dividends regularly and carry on every day operations easily.

The fixed assets has increased to ₹9506 crore, as company is investing a lot in expanding beds, medical equipments, land acquisitions for new hospital branches.

Cash Flow Analysis

Cash flow from Operations is positive for many years and in FY24 it is ₹1122 crore.

The Company has purchased fixed assets worth ₹786 crore in FY24, shows a great sign of expansion.

Max Healthcare has now started paying dividends to its shareholders as it has now enough cash reserves.

State Bank of India: A Leading Multinational Banking Institution

Established on July 1, 1955, following the nationalization of the Imperial Bank of India, the State Bank of India (SBI) is India’s largest multinational public sector bank, headquartered in Mumbai. Formed with the Reserve Bank of India initially acquiring a 60% stake, SBI has grown into a cornerstone of the Indian financial system.

SBI offers a comprehensive range of financial solutions through four primary segments: Treasury, Corporate/Wholesale Banking, Retail Banking, and Other Banking Business. Its extensive network, consisting of over 22,000 branches across India and 227 international offices in 30 countries, supports global financial operations from hubs like New York, Tokyo, and London. As a leader in digital innovation, SBI has introduced initiatives like SBI e-tax for online tax payments and the Virtual Debit Card, enhancing customer security and convenience.

The bank has experienced significant growth and expansion through strategic acquisitions, notably the 2017 merger with five associate banks and the Bharatiya Mahila Bank, which solidified its domestic dominance. Internationally, SBI has forged global collaborations, including a Payments Bank partnership with Reliance Industries and ventures with Visa and Elavon for merchant acquiring services. Its subsidiaries, such as SBI Life Insurance, a joint venture with Cardif S.A., and SBI Funds, recognized as ‘Mutual Fund of the Year,’ underscore its excellence in insurance and asset management.

SBI actively supports national development initiatives through specialized products like the Defence Salary Package and senior citizen loans. By leveraging technology-driven services, it ensures seamless financial solutions for customers across both urban and rural areas. With its strong domestic foundation and growing international presence, SBI continues to cement its role as a leader in the global banking sector.

Returns Summary

YTD

1 Month

6 Month

1 Year

2 Year

3 Year

5 Year

33.02%

4.01%

-5.72%

49.33%

40.56%

80.46%

154.00%

Result Highlights

State Bank of India (SBI) demonstrated a strong performance in Q2FY25, showcasing growth in profitability, business expansion, asset quality, and digital transformation. The bank reported a Net Profit of ₹18,331 crores, reflecting robust earnings. Key profitability metrics like Return on Assets (ROA) at 1.13% and Return on Equity (ROE) at 21.78% for H1FY25 underscore efficient capital utilization, while the Net Interest Margin (NIM) of 3.18% (3.31% domestic) highlights sustainable profitability.

SBI’s business growth remained impressive, with deposits crossing ₹51 trillion, up 9.13% YoY, and advances exceeding ₹39 trillion, registering a 14.93% YoY growth. This reflects balanced expansion across deposits and credit segments, positioning SBI for competitive market share growth. Asset quality improved significantly, with Gross NPA at 2.13% and Net NPA at 0.53%, supported by a Provision Coverage Ratio (PCR) of 75.66%, rising to 92.21% when including AUCA. Additionally, the bank maintained conservative provisioning, setting aside ₹31,084 crores, equivalent to 153% of Net NPAs, ensuring resilience against potential losses.

SBI’s digital transformation continues to lead, with >98% of transactions via alternate channels and over 8.13 crore users on its YONO app. Notably, 61% of savings accounts were opened digitally in Q2FY25, highlighting the platform’s pivotal role in customer acquisition and engagement. The bank’s liability franchise benefits from its 22% market share in deposits, with 10.05% YoY growth in current account balances, and a credit-to-deposit ratio of 67.87%, reflecting healthy lending activity.

To support future growth, the Central Board approved raising up to ₹20,000 crores in long-term bonds in FY25. This capital infusion, through public or private placement, will enhance the bank’s capital base, supporting its strategic goals of credit expansion and financial stability, while sustaining a balanced credit-to-deposit ratio. These initiatives position SBI for stable, long-term growth in a competitive banking landscape.

Shareholding Pattern

Return Comparison with Peers

Company

ROCE

6 Months

1 Year

3 Year

5 Years

State Bank of India

6.16%

4.53%

43.59%

21.75%

20.49%

Bank of Baroda

6.33%

-5.34%

21.77%

42.16%

20.01%

Punjab National Bank

5.46%

-12.86%

28.92%

41.02%

11.63%

IOB

5.41%

-18.30%

32.48%

37.16%

39.38%

Union Bank of India

6.55%

-12.79%

10.39%

39.99%

16.74%

Canara Bank

6.63%

-10.92%

23.11%

36.54%

19.29%

Indian Bank

5.92%

6.88%

41.61%

59.60%

36.32%

SBI Outlook and Contribution to Industry

State Bank of India (SBI) stands as a cornerstone of the Indian banking sector, with a ₹52 lakh crore balance sheet and a 22% market share in deposits. It dominates segments like home loans (26.5%) and auto loans (19.8%), supported by its 22,000 domestic branches and operations in 30 countries. SBI’s YONO digital platform drives innovation, handling 66 crore transactions annually, reflecting its leadership in technology-driven banking.

The industry outlook for FY25 and beyond is positive, with GDP growth at 6.7% in Q1 FY25, stable global conditions, and robust banking sector projections of 11-12% deposit growth and 12-13% credit growth. SBI leads this momentum, achieving ₹51.17 trillion in deposits and 14.93% credit growth YoY, backed by a strong capital adequacy ratio of 13.76% and high asset quality (Gross NPA at 2.13%).

Digital transformation remains a key driver, with over 8 crore digital users and 61% of savings accounts opened digitally in Q2 FY25. Its subsidiaries, such as SBI Life Insurance and SBI Funds, diversify its revenue streams, bolstering financial stability.

SBI’s focus on sustainable growth, digital innovation, and robust asset management positions it to capitalize on India’s economic momentum, ensuring long-term leadership and enhanced shareholder value.

Balance Sheet Analysis

SBI’s balance sheet from FY20 to FY24 shows steady expansion in key financial areas. Deposits grew from ₹32,74,160.63 crores to ₹49,66,537.49 crores, reflecting the bank’s strong customer base and competitive edge in attracting funds. Simultaneously, advances saw a significant rise, from ₹23,74,311.18 crores to ₹37,84,272.67 crores, driven by robust growth across corporate, retail, and MSME sectors. The bank has also shown consistent growth in reserves, increasing from ₹2,50,167.66 crores to ₹4,14,046.71 crores, indicating a strong capital base to support long-term sustainability. Borrowings grew from ₹3,32,900.67 crores to ₹6,39,609.50 crores, signifying

SBI’s use of external funding to drive its growth. While this increase reflects SBI’s expansion, effective asset-liability management remains critical. Investments and other assets also rose significantly, supporting SBI’s diversified portfolio. The net block remained stable, reflecting a balanced approach to capital expenditure in fixed assets. With strong asset growth and prudent liability management, SBI is well-positioned for continued market leadership in India’s banking sector, strengthened by its digital transformation through platforms like YONO.

Cash Flow Analysis

SBI’s cash flow analysis from FY2013 to FY2024 reveals significant fluctuations in its operational, investing, and financing activities. Operating cash flows have been largely positive, with notable spikes in FY2017 (+₹77,406 crores) and FY2022 (+₹89,919 crores), reflecting strong operational efficiency. However, negative flows in FY2018 and FY2023 highlight challenges such as higher provisioning for bad loans. In terms of investing activities, cash flows have consistently been negative, with the bank investing heavily in growth, technology, and acquisitions. A rare positive period in FY2018 likely reflects asset disposals. Financing activities show volatility, with positive cash inflows in certain years due to capital raising and negative flows in others, such as FY2024, likely reflecting debt repayments and a focus on capital strengthening. Despite these fluctuations, SBI has managed to maintain positive net cash flow in key years, ensuring liquidity for growth. Overall, SBI’s cash flow patterns reflect strategic financial management, including debt reduction and investment in expansion, positioning it for long-term growth.

Japanese companies, recognized globally for their advanced expertise in semiconductor technologies, are eager to establish manufacturing units in India, according to a report by Deloitte. This collaboration follows a significant memorandum signed between India and Japan, aimed at fostering joint development of the semiconductor ecosystem. Japan, with its robust semiconductor manufacturing infrastructure and as a global leader in semiconductor-related materials and equipment, is positioning itself as a key partner in India’s semiconductor ambitions.

Key Highlights of the Agreement:

Collaborative Development: The memorandum includes collaboration on semiconductor design, manufacturing, research, and talent development, ensuring a resilient global supply chain.

Japan’s Expertise: Japan’s ecosystem boasts over 100 manufacturing plants and leadership in semiconductor wafers, chemicals, gases, and other critical materials.

India’s Aspiration: India aims to establish 10 semiconductor plants within the next decade, aligning with its vision to become a global hub for electronics manufacturing.

Impact on the Indian Stock Market:

Boost for Technology Stocks: Companies in electronics, manufacturing, and semiconductor-related fields could see increased investor interest and capital inflows.

Opportunities in Ancillary Industries: Firms producing materials such as silicon wafers, chemicals, and chip-making equipment may experience growth.

Policy Incentives: Continued government support for the semiconductor industry, through subsidies and policy measures, is expected to enhance investor confidence in related sectors.

Global Recognition: India’s role in the semiconductor supply chain could attract more foreign direct investment (FDI), benefiting the broader market.

Strategic Implications:

Enhanced resilience in the global semiconductor supply chain, reducing dependence on single markets like China.

Opportunities for Indian talent to integrate into global semiconductor research and development.

Strengthened bilateral ties between India and Japan, promoting further economic cooperation.

The partnership highlights India’s growing prominence in the semiconductor domain, offering significant opportunities for domestic firms and international players to contribute to the country’s technological and economic growth.