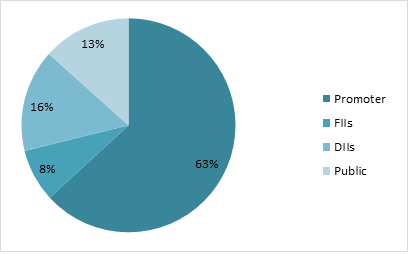

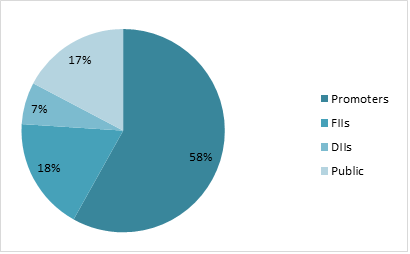

HDFC AMC Q3FY24: A Leading Player in India’s Mutual Fund Industry with 39.2% Revenue Growth

HDFC AMC Ltd: Overview

HDFC Asset Management Company (HDFC AMC) is one of India’s leading asset management companies and a prominent player in the mutual fund industry. Established in 1999, it operates as a joint venture between Housing Development Finance Corporation (HDFC). HDFC AMC offers a diverse portfolio of investment products, including equity, debt, hybrid, and liquid mutual funds, catering to retail and institutional investors. HDFC AMC has built a strong distribution network comprising banks, financial advisors, and digital platforms, ensuring its reach across urban and rural markets. With a focus on investor education and digital innovation, HDFC AMC continues to enhance customer experience and expand its market share. With a total AUM (Assets under Management) of approximately ₹46 lakh crore as of FY24, the industry is expected to grow at a CAGR of 12-15% in the coming years. Technology-driven platforms and robo-advisors are simplifying the investment process, encouraging more investors, especially from tier-2 and tier-3 cities. India’s growing economy and expanding middle class are fuelling demand for wealth management and investment products. The Indian AMC industry is poised for continued growth as the population becomes more financially savvy, disposable incomes rise, and markets deepen. With a strong track record, trusted brand, and focus on innovation, HDFC AMC is well-positioned to capitalize on these trends and maintain its leadership in the industry.

Business Segments:

- Mutual Fund: HDFC AMC manages a comprehensive suite of mutual fund schemes, catering to various investment needs, risk appetites, and time horizons. In equity funds for focused on long-term capital appreciation by investing in equity and equity-related instruments. Debt funds for designed to provide stable returns by investing in fixed-income securities like bonds, treasury bills, and money market instruments.

- PMS and AIFs: The Company offers customized portfolio management services for high-net-worth individuals (HNIs) and institutional clients. These services are tailored to specific investment goals and include active equity and fixed-income portfolio strategies. It manages alternative investment funds, catering to sophisticated investors seeking higher returns through non-traditional investment avenues like private equity, real estate, or venture capital.

- Other Products & Services: HDFC AMC manages retirement-focused funds under the National Pension System (NPS). Encourages regular investments by retail investors, fostering disciplined saving habits. Provides a platform for investors to invest directly in funds, bypassing intermediaries, and reducing costs.

Subsidiary Information:

- HDFC AMC International (IFSC) Ltd: The business of acting as an Investment Manager to the scheme(s) to be launched under AIFs, from time to time. Further, as a part of reward strategy for attracting new talents and retaining the existing resources holding critical roles required for the business of WOS, it is proposed to extend the benefits and coverage of the Scheme to present and future eligible employees of the WOS.

Q2 FY25 & Business Highlights

- Revenue of ₹935 crore in Q3 FY25 up by 39.2% YoY from ₹671 crore in Q3 FY24.

- EBITDA of ₹764 crore in this quarter at a margin of 82% compared to 76% in Q3 FY24.

- Profit of ₹641 crore in this quarter compared to a ₹488 crore profit in Q3 FY24.

- Total AUM of ₹7764 billion is handled by HDFC AMC and the live account are 22.1 million in Q3 FY25.

- The Debt market’s closing AUM is ₹1565 billion which is 13.2% increase YoY & Liquid market of ₹767 billion with increase of 14.2%.

- The channel distribution share of total AUM is MFDs 26.6%, National Distributors 21.3%, Direct 41.4%, HDFC Bank 5.7% and other Banks with 10.6% of total AUM share.

- HDFC AMC has total 280 offices out of which 196 are in B-30 locations and it contributes about 12% of share in market.

Financial Summary

| INR Cr. | Q3 FY24 | Q3 FY25 | FY23 | FY24 |

| Revenue | 671 | 935 | 2478 | 3160 |

| Expenses | 162 | 171 | 550 | 627 |

| EBITDA | 509 | 764 | 1929 | 2533 |

| OPM | 76% | 82% | 78% | 80% |

| Other Income | 143 | 93 | 4 | 4 |

| Net Profit | 488 | 641 | 1423 | 1943 |

| NPM | 72.7% | 68.6% | 57.4% | 61.5% |

| EPS | 22.9 | 30 | 66.7 | 91 |