Suzlon is a leading global provider of renewable energy solutions and a vertically integrated manufacturer of wind turbine generators (WTGs). The company’s operations span the design, development, and manufacturing of key components, including rotor blades, tubular towers, generators, control systems, gears, and nacelles. Additionally, Suzlon offers operation and maintenance (O&M) services in both India and international markets. As a comprehensive renewable energy solutions provider, Suzlon is involved in manufacturing, project execution, and O&M of wind turbine generators, along with the sale of related components. With over 20 GW of wind energy installations across 17 countries and 111+ wind farms in India boasting a total capacity of 13,880 MW, the company has a strong global footprint. Revenue contributions include ~73% from the sale of wind turbines and components, and ~27% from O&M services.

Latest Stock News (3 January 2025)

CRISIL has upgraded Suzlon energy Ltd rating for loan of ₹3050 crores, long term rating A and short term rating of A1. It was the second time, CRISIL has updated the ratings. Income Tax Appellate Tribunal (ITAT) has decided the quantum appeal in favour of the company and JAO has cancelled the penalty order of ₹87.59 crore. In total the total penalty amount levied by National Faceless Penalty Centre, Income Tax Department is ₹260.3 crores. The CEO of SE Forge Ltd a wholly owned subsidiary of the Company has resigned from the position.

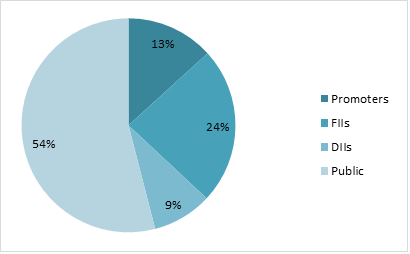

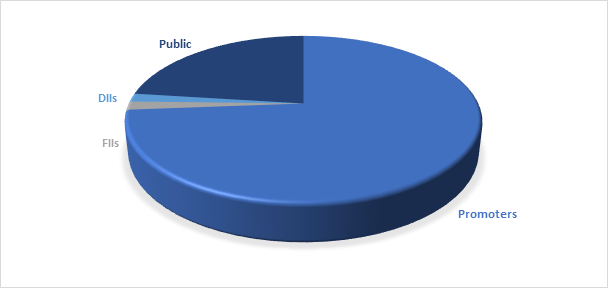

Shareholding Pattern as on September 2024

Key Stats

Market Cap

₹83849 Crore

Revenue

₹7881 Crore

Profit

₹986 Crore

ROCE

24.93%

P/E

85

Peer Comparison

Amt in ₹ Cr

MCap

Sales

PAT

ROCE

Asset Turn.

EV/EBITDA

D/E

P/E

Suzlon Energy

83849

7881

986

24.93%

1.03

62.65

0.06

85

CG Power & Ind.

112609

8810

896

46.63%

1.56

85.9

0.01

125.6

Hitachi Energy

64105

5850

199

17.85%

1.21

155.6

0.25

321.4

Premier Energies

59750

3143

231

25.3%

1.11

116.8

0.55

254

Triveni Turbines

24755

1854

315

38.5%

1.09

53.6

0.01

78.4

Financial Trends

Amount in ₹ Cr

2020

2021

2022

2023

2024

Revenue

2973

3346

6582

5971

6529

Expenses

3829

2809

5682

5137

5492

EBITDA

-856

537

900

833

1037

OPM

-29%

16%

14%

14%

16%

Other Income

-42

823

95

2739

-26

Net Profit

-2692

104

-177

2887

660

NPM

-90.5%

3.1%

-2.7%

48.4%

10.1%

EPS

-4.01

0.1

-0.17

2.28

0.49

Stock Price Analysis

In terms of performance, Suzlon Energy has shown a return of -5.27% over the past month, and -18.2% in the last three months. Over the past 52 weeks, the shares have seen a low of ₹35.49 and a high of ₹86.04. The trades’ volumes have increased greatly and stock has also increased significantly indicating high volatility. The stock price now is at resistance level and might see some setbacks in coming weeks.

Sundaram Finance Ltd was established in 1954, with the business of financing the purchase of commercial vehicles and now it has diversified into many other segments like home finance, Mutual funds, general insurance, financial service distribution, etc. It has subsidiaries for different work segments like India Equipment Leasing Ltd, Sundaram Home Finance Ltd. It had a total of 680+ branches and as a group they had 1050+ branches worldwide. They have 671 branches for Asset Finance, 117 for Home Finance, 164 for General Insurance and 85 for Mutual Funds. They also have diesel finance and tyre finance to pay in 3-6 instalments. The total group AUM stood at 108,000 crore and 34,500 crore is under asset finance and 54,800 under AMC business. Sundaram Finance Ltd has risen term funding of ₹8000 crore from Banks, Mutual funds and Insurance companies.

Stock News

Sundaram Home Finance Ltd has announced plans to expand its presence in tier-3 towns in western Tamil Nadu under its ‘Emerging Business’ segment, citing strong growth potential. Currently it handles overs 15 branches in that region and aims to disburse ₹500 crore in next 12-18 months, with ₹50 crore targeted to specifically with EB. This move follows the successful launch of its Coimbatore branch. The Pollachi branch will offer small business loans of up to Rs 20 lakh to entrepreneurs for working capital and business growth. It will also target the affordable housing finance market, offering loans of up to Rs 35 lakh.

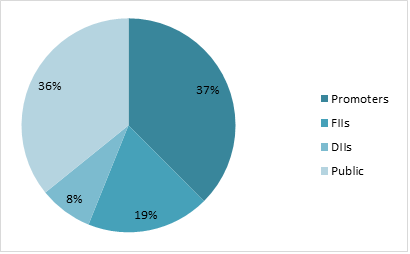

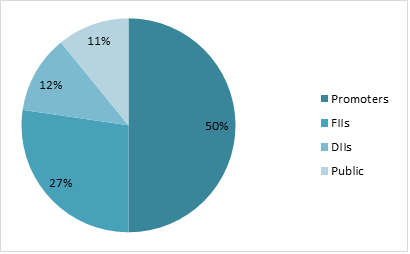

Shareholding Pattern as on September 2024

Key Stats

Market Cap

₹51726 Crore

Revenue

₹8013 Crore

Profit

₹1603 Crore

ROCE

9.21 %

P/E

32.26

Peer Comparison

Amt in ₹ Cr

MCap

Sales

PAT

ROCE

Asset Turn.

EV/EBITDA

D/E

P/E

Sundaram Fin.

51718

8013

1603

9.21%

0.12

16.85

4.5

32.27

Shriram Fin.

114517

38466

7839

11.3%

0.16

11.08

3.97

14.57

Muthoot Fin.

89907

14397

4413

13.2%

0.16

13.64

2.82

20.34

L&T Fin.

35468

15009

2573

8.22%

0.13

12.58

3.5

13.8

Chola Fin.

29156

29603

2054

10.73%

0.17

10.33

13.85

14.24

Financial Trends

Amount in ₹ Cr

FY2020

FY2021

FY2022

FY2023

FY2024

Revenue

4707

5292

5111

5501

7274

Expenses

3649

3894

3628

3695

5050

EBITDA

1058

1398

1483

1806

2224

Financing Margin %

22%

26%

29%

33%

31%

Net Profit

845

1223

1296

1510

1842

NPM

18.0%

23.1%

25.4%

27.4%

25.3%

EPS

71.25

104.7

105.6

119.5

129.3

Stock Price Analysis

Sundaram Finance Ltd.’s share price is experiencing a bullish surge today, rising by approximately 8.5%. As of January 2, 2025, the stock opened at ₹4,125.65 and reached a high of ₹4,418.80 during intraday trading. This increase comes on the heels of a challenging week, where the stock had previously dropped by 7.08%. The current trading volume stands at 354,146 shares, reflecting robust investor interest. From a technical standpoint, Sundaram Finance’s stock is currently navigating through significant resistance levels. The 52-week low is recorded at ₹3,447.00, while the 52-week high stands at ₹5,535.85.

When Jai Corp Limited was first established on June 6, 1985, it produced a variety of goods, including spun yarn, PP Staple Fiber, FIBC Jumbo Bags, woven bags and fabrics, and geotextiles. Since then, businesses have expanded into real estate development, coils, and sheets of CR steel.

As time went by, the company diversified into areas such as SEZ development, infrastructure projects, venture capital, and investment advisory services, reflecting the ability to adapt to opportunities that emerged. The company started its commercial production in 1987 with an HDPE/PP Woven Sacks manufacturing unit at Murbad, Maharashtra. The company then further expanded in 1990 and 1992 with other facilities. During the years, Jai Corp restructured itself several times. Notably, it changed its name from Jai Fibres Ltd to Jai Corp Limited in 1994 and also acquired subsidiaries in 2007 to enhance its presence in the venture capital and infrastructure sectors. To demonstrate its infrastructure-oriented strategy, Jai Corp established SPVs for electricity generation, transmission, and distribution in SEZ areas. In 2007–2008, the company ventured into the international market of real estate by incorporating a subsidiary in Mauritius. The group dissolved its Section 8 trust and merged its subsidiary, Jai Realty Ventures, with the aim to concentrate on its core business and streamline operations.

Financial history indicates significant preference shares redemption in focus by Jai Corp. Some examples include between 2014 to 2019, there were several tranches of preference shares redeemed at premium with shareholder approvals for periodic rollover. In 2020, it was an order from National Company Law Tribunal approving the amalgamation of Jai Realty Ventures with the parent company to simplify corporate structure. The firm has also shown resilience under the COVID-19 pandemic where it managed to reopen facilities in stages and ended non-core operations such as spinning during 2020.

Latest News (02-Jan-2025)

Shares of Jai Corp Ltd gained 3% on August 27 after the NCLT approved the merger of promoter company Pet Fibres with Mega Pipes. Following the merger, Pet Fibres’ 2 lakh equity shares (0.2% stake) in Jai Corp will be transferred to Mega Pipes.

Shareholders are advised to update or transfer their Depository Participant (DP) account details as shares in Pet Fibres’ DP account with ILFS will move to Mega Pipes’ DP account with MOSL.

Jai Corp, established in 1985, is a diversified manufacturer specializing in steel, plastic processing, and spinning yarn, while expanding into SEZs, infrastructure, venture capital, and real estate.

In its April-June earnings, Jai Corp reported a 4.56% YoY increase in revenue and a 148% YoY surge in net profit. The Board is set to meet on August 29 to discuss a potential share buyback.

As of 12:10 pm, Jai Corp shares were trading 0.745% higher at ₹389.50 on the NSE.

Returns Summary

YTD

1 Month

6 Month

1 Year

2 Year

3 Year

5 Year

-24.15%

-33.72%

-39.77%

-37.89%

63.20%

101.46%

154.00%

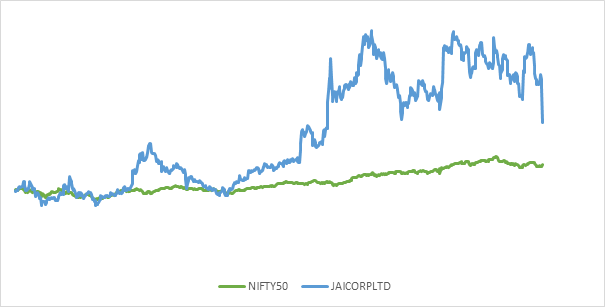

3 Years Return: Jai Corp Ltd. v/s Nifty 50

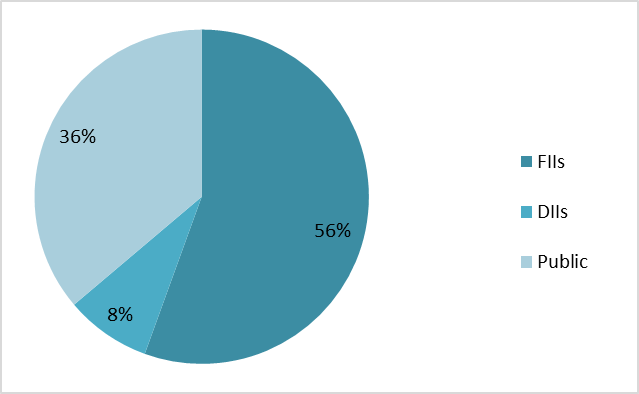

Shareholding Pattern

Key Metrics

Metrics

–

Mkt Cap (INR Cr):

4,441 Cr.

52-week H/L:

438/248

PE Ratio:

66.46

Dividend yield:

0.20%

ROCE:

3.81%

P/B:

2.98

NSE Code:

JAICORPLTRD

Financial Trends

Year

Sales (₹ Cr)

Operating Profit (₹ Cr)

OPM (%)

Net Profit (₹ Cr)

EPS (₹)

Reserves (₹ Cr)

Borrowings (₹ Cr)

Fixed Assets (₹ Cr)

Debt/Equity

Mar-18

588

63

11%

-1

-0.11

1,104

622

274

0.56

Mar-19

636

71

11%

-108

-6.06

1,016

580

279

0.57

Mar-20

527

45

9%

34

1.88

1,048

470

256

0.45

Mar-21

472

48

10%

93

5.19

1,139

330

230

0.29

Mar-22

720

55

8%

53

2.95

1,197

236

224

0.2

Mar-23

594

44

7%

-14

-0.76

1,178

239

225

0.2

Mar-24

463

48

10%

52

2.94

1,233

236

213

0.19

Peer Comparison

Company

Price (Rs.)

MCAP (Cr.)

P/B

P/E

EPS (Rs.)

ROE (%)

ROCE (%)

P/S

EV/EBITDA

Jai Corp

247.9

4,441.00

2.98

66.46

4.13

3.98

3.81%

9.52

44.12

EPL

263.5

8,361.67

8.51

39.86

6.58

19.84

18.6

6.53

23.5

Responsive Inds

262.65

6,902.50

7.37

206.02

1.26

3.48

5.6

10.54

63.87

Shaily Engg. Plastic

1,511.70

6,848.56

15.25

167.64

8.89

8.75

11.07

11.12

63.42

Jain Irrigation Sys

74.42

4,984.55

1.03

391.32

0.19

1.19

5.08

1.3

16.53

Prince Pipes & Fitti

430.35

4,754.68

3.02

36.11

11.91

12.55

16.25

1.85

16.88

Polyplex Corporation

1,369.40

4,299.20

6.27

5,243.11

0.26

-1.33

-1.36

3.04

83.13

Jindal Poly Films

976.4

4,260.20

0.69

8.52

114.21

5.53

7.3

7.84

7.63

Kingfa Science

3,471.00

4,159.94

6.37

30.99

110.83

23.24

30.26

2.8

20.39

Xpro India

1,532.90

3,410.24

5.74

71.12

21.62

12.29

15.04

7.33

39.97

Stock Analysis

Jai Corp. Ltd. is a diversified company operating in the steel industry. Plastic production and ownership Facing a growing market trend, on January 2, 2025, Urban Infrastructure Holdings Private Limited (UIHPL) fell 19.99 % to ₹248.40 due to planned capital reduction by Jai Corp. over the last five years. The company’s sales growth was very negative at -6.14%, indicating problems with generating income. It is reported to be low. This may raise concerns among investors about the company’s ability to create dust in the stock market. The sudden change in the share price is the result of UIHPL’s planned capital reduction, which has raised concerns about the impact on Jai Corp’s financial health and future cash flows. Considering the new market reaction and related economic factors. Investors should be watchful: High P/L ratio signals that a stock may be overvalued. Negative output growth over five years indicates a structural situation. According to the report, UIHPL’s equity market is under uncertainty that would affect Jai Corp’s financial position. Some reported lower quarterly earnings and revenue. Broader economic indicators and current market conditions suggest caution. An investor should not scrutinize the financial condition and history of a company before investing.

Considering all these factors investors are recommended to remain watchful as mentioned in the above para. Don’t invest until some major changes happens in the company’s operation. Wait for the right time to make entry!

In 1998, Petronet LNG Ltd. was established to oversee the planning, building, and operation of LNG import and regasification terminals, hence playing a crucial role in India’s energy sector. GAIL, Indian Oil Corporation (IOCL), Bharat Petroleum (BPCL), and ONGC formed the joint venture, each with an equal 12.5% share. It runs two main terminals, one in Dahej, Gujarat, with a capacity of 17.5 MMTPA and another in Kochi, Kerala, with a capacity of 5 MMTPA, for a total of 22.5 MMTPA. The majority of its revenue, around 95%-96%, comes from LNG sales, with the remaining 3%-4% from regasification services. GAIL, IOCL, and BPCL are key customers, accounting for about 95% of total revenue. Petronet is building a new LNG terminal at Odisha, with an initial capacity of 4 MMTPA and an estimated investment of ₹2,300 crore, as part of its infrastructure expansion to further solidify its position. The corporation is also increasing the storage and regasification capacities of its existing terminals. Furthermore, Petronet is expanding into the Green Hydrogen value chain, demonstrating its commitment to innovation, sustainability, and alignment with global clean energy trends.

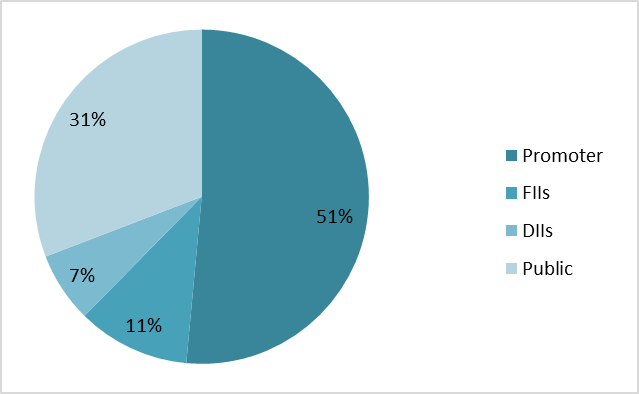

Shareholding Pattern as on September 2024

Key Stats

Market Cap

₹49190 Crore

Revenue

₹54977 Crore

Profit

₹3917 Crore

ROCE

26.41%

P/E

12.56

Peer Comparison

Amt in ₹ Cr

MCap

Sales

PAT

ROCE

Asset Turn.

EV/EBITDA

D/E

P/E

Petronet LNG

49190

54977

3917

26.41%

2.22

6.67

0.15

12.56

GAIL

125577

136080

11534

14.66%

1.15

7.25

0.23

10.89

Adani Total Gas

80845

4687

702

21.2%

0.73

66.3

0.37

115.3

Gujarat Gas

34970

16295

1225

20.51%

1.39

15.36

0.02

28.55

Mahanagar Gas

12802

6437

1149

36.6

0.94

6.85

0.03

11.14

Financial Trends

Amount in ₹ Cr

2020

2021

2022

2023

2024

Revenue

35452

26023

43169

59899

52729

Expenses

31462

21323

37918

55045

47520

EBITDA

3990

4700

5250

4854

5209

OPM

11%

18%

12%

8%

10%

Other Income

306

377

395

523

605

Net Profit

2703

2939

3438

3326

3652

NPM

7.6%

11.3%

8.0%

5.6%

6.9%

EPS

18.02

19.59

22.92

22.17

24.35

Stock Price Analysis

The stock has not given any return in phase of 2017 to 2023, it was in consolidation and broke it and now it is trading at around its high level of ₹340 per share. The volume of shares traded has lowered these days compared to years in history. The stock might fall a little on basis of technical analysis for couple of months.

Latest Stock News (2 January 2025)

Petronet LNG Ltd. clarified that LNG terminal regulation does not fall under the PNGRB’s purview without amendments to the 2006 Act. The company highlighted its competitive regas charges, which constitute only 5-6% of delivered gas prices.

However, PNGRB’s recent paper criticized rising regas charges despite capacity expansion at the Dahej terminal, suggesting the need for regulatory oversight to ensure fair pricing. Foreign brokerage Citi flagged regulatory risks, issuing a “Sell” rating with a ₹310 target. Petronet shares dropped 5.49% to ₹328.50, signaling a negative start to 2025 after a 45% gain in 2024.

TVS Holdings Ltd was established in 1962 as a Sundaram Clayton Ltd in Chennai by Venu Shrinivasan. Today it is known as TVS Holdings. It is a largest manufacturer of auto components and distribution groups in India. It is a leading supplier of aluminium die castings to automotive and non-automotive sectors. It makes aluminium castings for two wheelers, heavy commercial vehicles, passenger cars, etc. The export revenue contributes 26% in the total revenue. It has about 27 subsidiaries and 3 associate companies. It holds approximately 50% of TVS Motor Company Ltd. which is engaged in 2/3 wheelers segment. It also holds TVS Credit Services Ltd a retail finance firm also providing finance to TVS Motors. It has also acquired 50% of stake in Sundaram Holding USA Inc. The company has 5 manufacturing plants four in Tamil Nadu and one in USA, and is planning to expand to meet the additional demand from market.

Shareholding Pattern as on September 2024

Key Stats

Market Cap

₹19020 Crore

Revenue

₹42168 Crore

Profit

₹952 Crore

ROCE

14.98%

P/E

19.8

Peer Comparison

Amt in ₹ Cr

MCap

Sales

PAT

ROCE

Asset Turn.

EV/EBITDA

D/E

FCF

TVS Holdings

19020

42168

952

14.98%

0.96

6.76

8.24

-1341

Bajaj Holdings

132513

1732

7407

13.07%

0.03

17.3

0.00

1941

Cholaman.Inv.&Fin.

104535

22502

3851

10.41%

0.45

15.58

7.38

-36754

Maha. Scooter

11006

182

175

0.88%

0.01

65.28

0.00

206

Sundaram Fin. Hold

6771

315

571

5.85%

0.07

24.1

0.00

132

Financial Trends

Amount in ₹ Cr

2020

2021

2022

2023

2024

Revenue

19858

20299

25591

33662

40248

Expenses

17446

17911

22599

29356

34417

EBITDA

2412

2388

2992

4306

5830

OPM

12%

12%

12%

13%

14%

Interest

910

929

985

1424

2043

Net Profit

627

592

824

1333

1782

NPM

3.2%

2.9%

3.2%

4.0%

4.4%

EPS

166.89

160.24

218.31

321.16

396.23

Stock Price Analysis

The prices of stock before 2014 were in range of ₹300 per share which now rose to high of ₹15,000 level. From 2015-2022 was the consolidation phase and after breaking it the stock has ran about 4 time to now reaching its all-time high. The stock has now seen a minor setback in its prices and it is trading at ₹ 9500 per share level. The volatility is increased and so the volumes of share traded every day compared to past.

Latest Stock News (2 January 2025)

TVS Holdings Ltd acquired a 100% stake in TVS Digital Ltd (formerly TVS Housing Ltd) from TVS Motor Company Ltd for ₹4.14 crore. This acquisition, a related party transaction conducted at arm’s length, makes TVS Digital a wholly-owned subsidiary. Headquartered in Chennai, TVS Digital operates in IT services and reported a turnover of ₹3.85 crore with a net profit of ₹0.27 crore in FY 2023-24. The move aligns with TVS Holdings’ strategy to consolidate non-automotive investments. Shares of TVS Holdings closed at ₹14,205, down 0.35% on the NSE.

One 97 Communications Ltd is a parent entity of Paytm, which was founded in 2000 by Vijay Shekhar Sharma. It is a one of leading payments and financial service platform which has transformed the business offerings in range of digital solutions to customers, merchants and enterprises. In digital payment segment it provides wallet based transactions, UPI, and POS merchant solutions. It provides loans, insurance, wealth management services through its platform. It has newly introduced Paytm Soundbox for merchants and small enterprises. In 2023, it partnered with Amadeus for travelling and ticket booking businesses. The main negative points of company are that its marketing expense is really high and is not performing its operations in compliance with RBI.

Shareholding Pattern as on September 2024

Key Stats

Market Cap

₹62922 Crore

Revenue

₹8278 Crore

Profit

₹-2013 Crore

ROCE

-8.4%

P/E

–

Peer Comparison

Amt in ₹ Cr

MCap

Sales

PAT

ROCE

Asset Turn.

EV/EBITDA

D/E

FCF

One 97 Comm.

62972

8278

-2013

-8.5%

0.57

-47.3

0.01

-161

One Mobikwik

4695

875

14.3

8.96%

1.12

121.17

1.38

-27.6

Info Edge

112819

2662

483

3.65

0.1

86.63

0.01

673

Just Dial

8566

1100

311.6

4.81%

0.23

19.5

0.02

245

Financial Trends

Amount in ₹ Cr

2020

2021

2022

2023

2024

Revenue

3279

2801

4974

7990

9978

Expenses

5964

4640

7358

9634

10921

EBITDA

-2685

-1838

-2384

-1644

-943

OPM

-82%

-66%

-48%

-21%

-9%

Other Income

-45

356

288

410

314

Net Profit

-2958

-1701

-2369

-1776

-1422

NPM

-90.2%

-60.7%

-47.6%

-22.2%

-14.3%

EPS

-470.6

-280.4

-36.9

-28.03

-22.3

Stock Price Analysis

The share price has fallen from its IPO price of ₹1600 something to 370-400 per share levels, because of its overvaluation and not proper operations in compliance with RBI has affected the brand value among the retail customers. The share volumes have increased from the past as it has become more volatile stock because of constant news or trending in market. It is at resistance level and might fall from this level.

Latest Stock News

SoftBank has fully exited One97 Communications, the parent company of Paytm, by selling its remaining 1.4% stake. The Japanese conglomerate, which initially held an 18.5% stake during Paytm’s IPO in 2021, gradually reduced its holdings through open-market transactions. This marks the end of SoftBank’s investment in the fintech giant.

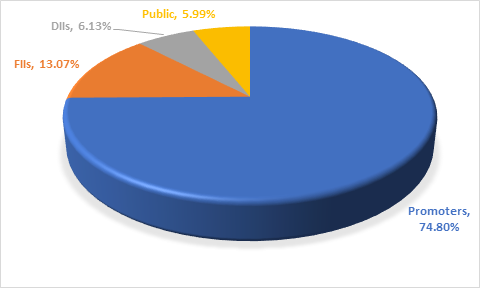

Bajaj Holdings & Invest. Ltd, was demerged from Bajaj Auto Ltd. The manufacturing work was transferred into Bajaj Auto, wind farm business and financial services business was given to Bajaj Finserv Ltd, and the properties, assets, liabilities of Bajaj Auto is transferred to Bajaj Holdings & Investments Ltd. It is registered as NBFC with RBI and it holds more than 35% stake in both Bajaj Auto Ltd and Bajaj Finserv Ltd. The revenue segments for the firm are basically interest income, fair value gain/loss and dividend income. The investments are done in Equity and debt markets; the diversification is handled as 65% investments in equity market and 35% in debt funds to balance the risk of its portfolio.

Shareholding Pattern as on September 2024

Key Stats

Market Cap

₹130761 Crore

Revenue

₹1732 Crore

Profit

₹7407 Crore

ROCE

13.07%

P/E

17.7

Peer Comparison

Amt in ₹ Cr

MCap

Sales

PAT

ROCE

Asset Turn.

EV/EBITDA

D/E

FCF

Bajaj Hold & Inv.

130761

1732

7407

13.07%

0.03

17.07

0.00

1941

Bajaj Finance

422635

62278

15373

11.92%

0.17

16.94

3.74

-73753

SBI Cards

63312

17749

2210

12.54%

0.33

17.05

3.3

-5526

Shriram Finance

108981

38466

7839

11.27%

0.16

10.87

3.97

-31635

Muthoot Finance

86144

14397

4133

13.15%

0.16

13.31

2.82

-9471

Financial Trends

Amount in ₹ Cr

2020

2021

2022

2023

2024

Revenue

435

457

484

522

1702

Expenses

134

106

117

142

140

EBITDA

301

352

367

380

1562

OPM

69%

77%

76%

73%

92%

Other Income

3058

3451

3896

4673

5967

Net Profit

3080

3654

4126

4946

7365

NPM

708.0%

799.6%

852.5%

947.5%

432.7%

EPS

268.8

327.98

364.5

435.8

652.7

Latest News

The Bajaj Group, home to some of India’s most prestigious companies, has consistently delivered exceptional value to its investors. Known for its strong fundamentals and reliable returns, the group has established itself as a powerhouse for long-term wealth creation.

With the highly anticipated IPO of Bajaj Housing Finance on the horizon, an analysis by ETMarkets highlights robust performance across the Bajaj Group’s diverse portfolio. Flagship companies such as Bajaj Finance, Bajaj Finserv, Maharashtra Scooters, and Bajaj Auto have achieved extraordinary growth, with stock prices soaring over 1000%, transforming early investors into millionaires.

Bajaj Finance stands out as a prime example, delivering a staggering 2876% return over the past decade. This impressive stock performance is underpinned by solid financial growth, including a profitability CAGR of 34% and sales CAGR of 29.8% between FY14 and FY24, making it one of the most celebrated stocks in the market.

Stock Price Analysis

The share price is in growing trend and is increasing before 2020 and is still rising because the company holds the Bajaj Auto Ltd and Bajaj Finserv Ltd and they have been doing well in the market. Since Covid-19, the stock has increased 7 times from that price levels. The share traded volumes are still normal but the financials are helping the stock prices reach at new higher levels.

Adani Total Gas Limited (ATGL), a joint venture between the Adani Group and TotalEnergies both owning 37.4 percent equity shares in the company, is one of the big players in CGD in India. The company’s primary operations include transportation gas supply and supply of natural gas for domestic, commercial and industrial purposes. ATGL commenced operations in 2004 and has grown to serve 34 districts while having equity stakes in a further 19 districts through a joint venture with the Indian Oil Corporation known as Indian Oil Adani Gas Pvt Ltd (IOAGPL). The cumulative distribution of Compressed Natural Gas (CNG) and Piped Natural Gas (PNG) with the active distribution of 577 CNG stations within the network by October 2024 remain the core businesses within its operations contributing positively to its operational finance. Consistent with its promise to sustainability, the company has diversified its operations into innovative energy solutions through its subsidiary Adani TotalEnergies E-Mobility Limited, focused on biogas, LNG, green hydrogen and electric vehicle infrastructure. Notwithstanding recent controversies sparked off by the allegations involving its parent company concerning corporate governance, ATGL rests the arguments on premises that the concerns surrounding their investment will lead to growth and therefore innovation which it has funding of $375 million sourced internationally to expand its distribution network across 13 states that is in line with India’s clean energy vision.

Returns Summary

YTD

1 Month

6 Month

1 Year

2 Year

3 Year

5 Year

-22.46%

-5.54%

-13.68%

-22.46%

-79.26%

-55.29%

371.14%

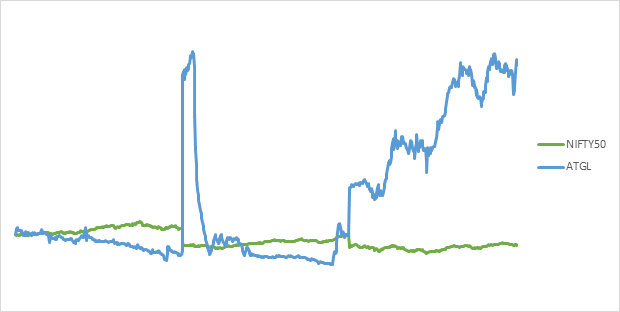

3Years Return: SBI Ltd. v/s Nifty 50

Shareholding Pattern

Key Metrics

Metrics

–

Mkt Cap (INR Cr):

83,230 Cr.

52-week H/L:

1198/546

PE Ratio:

120.81

Dividend yield:

0.03%

ROCE:

21.26%

P/B:

21.5

NSE Code:

ATGL

Financial Trends

Year

Sales (₹ Cr)

Operating Profit (₹ Cr)

OPM (%)

Net Profit (₹ Cr)

EPS (₹)

Reserves (₹ Cr)

Borrowings (₹ Cr)

Fixed Assets (₹ Cr)

Debt/Equity

Mar-18

1,374

366

27%

162

6.31

759

1,345

897

1.77

Mar-19

1,719

455

26%

229

2.08

992

394

980

0.4

Mar-20

1,875

595

32%

436

3.97

1,361

428

1,198

0.31

Mar-21

1,696

704

42%

463

4.21

1,824

529

1,379

0.29

Mar-22

3,038

773

25%

509

4.63

2,306

1,035

1,733

0.45

Mar-23

4,378

870

20%

546

4.97

2,831

1,422

2,335

0.5

Mar-24

4,475

1,104

25%

668

6.07

3,470

1,557

3,174

0.45

Peer Comparison

Company

Price (₹)

Market Cap (₹ Cr)

P/B

P/E

EPS (₹)

ROE (%)

ROCE (%)

P/S

EV/EBITDA

Adani Total Gas

761.05

83,701.05

21.5

120.81

6.3

20.09

21.26

18.72

69.58

Gujarat Gas

498.7

34,330.02

4.32

27.1

18.4

15.56

21.65

2.19

15

Indraprastha Gas

415.65

29,095.53

3.1

18.1

22.96

22.36

29.86

2.08

10.55

Gujarat State Petronet

361.9

20,418.81

1.93

18.16

19.93

13.15

16.86

10.05

11.88

Mahanagar Gas

1,284.40

12,687.02

2.29

11.04

116.37

27.79

37.6

2.03

6.71

Confidence Futuristic

89.7

224.43

1.6

83.78

1.07

1.86

2.63

44.36

58.09

Latest News

Adani Total Gas has reported a 7.2% revenue growth over the past year and an impressive 111% growth over three years. Despite industry-wide challenges, including a projected 5.1% revenue decline, the company has maintained resilience, justifying its elevated price-to-sales (P/S) ratio.

Investors remain optimistic about its ability to outperform peers, but future growth hinges on overcoming challenges like declining natural gas allocations. With revenue growth exceeding industry trends, Adani Total Gas continues to attract attention, though its ability to sustain this momentum will be crucial.

Stock Analysis

On December 31 2024 Adani Total Gas Ltd. Share price close in a market fall-down by 3.28% and made an intraday low at 726.6. This fall came on the heels of four consecutive days of gain and was in stark contrast to 2.46 percent fall (over the past month) with the Sensex. One of the major reasons for the drop is the decrease in APM-priced domestic gas allocation. In this regard GAIL India Limited vide letter dated November 15 2024, communicated to ATGL, a reduction in gas allocation by 13% effective from November 16 2024. Its relatively decrease affect all the City Gas Distribution CGD sector. It also expected to speak negatively of the firm about profits. Noting revenue, the last push could be rationalized on a standalone basis by ATGL is basically growing revenue in some form of consistent manner. This may lead investors speculate that revenues will come through hard and glaze in the coming period and allow sales annual growth. According to the consensus of analysts, the stock’s target price is ₹1,085.00, which means that it can potentially gain by around 59.72% from the last closing price of ₹679.30. The recent cuts on gas allocation and potential cuts on profitability should sway investors and affect stock performance in the near term, however. How quickly is still dependent on how ATGL manages these issues and tailors its approach to mitigate the effects of declining natural gas supplies. It is up to investors to closely watch and see what operational improvements ATGL makes on top of market developments to determine when a turnaround in the company’ stock performance will occur.

Investors are advised to keep their eyes on the companies’ financials and strategic decisions which will provide further direction as to take the appropriate action in short term. However, the future from long term perspective looks attractive.

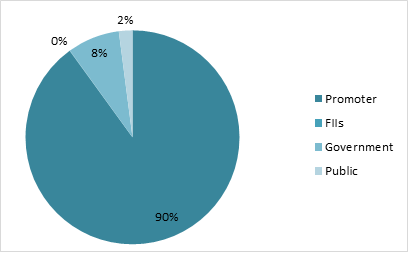

ITI is a government-owned company under the ministry of Communications which was established in 1948. Full form of ITI is India Telephone Industries. And it provides diverse range of telecom products and services. The revenue bifurcation of company is 78% Turnkey projects, 19% service projects and 3% manufacturing projects. The Company’s order book is filled with government tenders for network distribution and connection over full area under its state. Its clientele is BSNL, Mahanagar Telephone Nigam Ltd and Indian Defence services. The 74% of company’s revenue is accounted from PSUs. It has total 1600+ employees working under its company. And it has no export revenue, and no outside Indian company is its client. Whole revenue is from PSUs or Ministry of government.

Shareholding Pattern as on September 2024

ITI Ltd Key Stats

Market Cap

₹36,459 Crore

Revenue

₹1264 Crore

Profit

-₹569 Crore

ROCE

-8.35%

P/E

–

Peer Comparison

Amt in ₹

MCap

Sales

PAT

ROE

Asset Turn.

EV/EBITDA

D/E

FCF

ITI Ltd

36459 Cr

2396 Cr

(474 Cr)

-27.30%

0.13

-201.3

1.05

937 Cr

Astra Microwave

7155 Cr

969 Cr

130 Cr

15%

0.72

30.7

0.31

(229 Cr)

Tejas Network

20133 Cr

6260 Cr

454 Cr

2.06%

0.42

20.5

0.78

(2445 Cr)

Avantel

3692 Cr

229 Cr

61.7 Cr

39.20%

1.19

38.67

0.08

39.5 Cr

ADC India Comm.

752 Cr

179 Cr

21 Cr

33.70%

1.96

17.9

0

19.4 Cr

Financial Trends

Amount in ₹ Cr

FY 2020

FY 2021

FY 2022

FY 2023

FY 2024

Revenue

2059

2362

1861

1395

1264

Expenses

1914

2313

1753

1549

1582

EBITDA

144

50

107

-154

-318

OPM

7%

2%

6%

-11%

-25%

Net Profit

146

9

119

-360

-569

NPM

0.07

0.00

0.06

-0.26

-0.45

EPS

1.58

0.1

1.27

-3.79

-5.92

ITI Ltd Analysis

The share price of ITI was in consolidation phase from 2018 to 2023, but now it broke that phase and it’s at all time high levels. And on 30th December 2024 the share price rose by 15.5% reaching at ₹379 per share. Its 52 week High/Low is ₹404/210. The volatility very high in the stock, because in about 15 months the stock has given 3 times returns to its investors, showing a sign of high risk and volatility in future. Volumes in past months and in history were less than 2 million trades per day but since past 2 months the volumes have increased to 70-90 million trades per day.

News

ITI Limited has significantly improved its operational efficiency, reducing working capital requirements from 196 days to 15.1 days.

For Q2FY25, the company reported consolidated revenue of ₹1,016.20 crore, a substantial increase from ₹246.47 crore in the same quarter last year. Losses were also reduced to ₹70.10 crore, compared to ₹125.81 crore in Q2FY24.

The company, in partnership with its consortium, secured the lowest bidder position (L1) for two packages worth ₹3,022 crore under BharatNet Phase-3. These packages cover Himachal Pradesh, West Bengal, and Andaman and Nicobar Islands, focusing on designing, supplying, constructing, and maintaining the Middle Mile Network funded by the USOF.

ITI is already executing optical fiber projects worth ₹5,400 crore across Tamil Nadu, Maharashtra, and Gujarat under earlier BharatNet phases and serves as the Project Implementation Agency for MahaNet-I and Gujarat Fiber Grid Network Ltd.

The Aditya Birla Group’s main metals company, Hindalco Industries Limited, is a major producer of copper, one of Asia’s biggest producers of raw aluminum, and a world leader in the rolling and recycling of aluminum. Bauxite mining, alumina refinery, aluminum smelting, rolling, extrusion, and foil manufacturing are all parts of Hindalco’s operations in India. Its copper section, which produces copper rods and supplies more than half of India’s copper needs, including major contributions to Indian Railways, has a state-of-the-art bespoke smelter and captive jetty. Hindalco was founded on December 15, 1958, and began operations in 1962 with an initial capacity of 20,000 metric tons of aluminum metal and 40,000 metric tons of alumina in Renukoot, Uttar Pradesh. By 1965, the business had increased its rolling and extrusion downstream capabilities. To support its operations, the Renusagar Power Plant was put into service in 1968. A significant expansion, modernization, and diversification program was launched in 1994, laying the foundation for future growth. Hindalco ventured into aluminum foil production in 1998 with the establishment of its Silvassa plant. In 1999, it began manufacturing aluminum alloy wheels at the same location. During this time, the company’s capacity to produce Renukoot metal increased to 242,000 metric tons per year. Hindalco acquired a 74.6% share in the (Indal) in 2000. Hindalco is committed to growing its supply chain capabilities and develop innovative products. Hindalco broadened its product portfolio by introducing innovative solutions tailored to various industries, including telecommunications, air conditioning, and railways. Notably, it made history by launching India’s first aluminium freight rake in Odisha, marking a significant step in sustainable and efficient transport solutions. Hindalco is on the run to leave its remarkable footprints across the globe.

Returns Summary

YTD

1 Month

6 Month

1 Year

2 Year

3 Year

5 Year

0.50%

-6.59%

-9.85%

2.06%

31.18%

36.51%

186.91%

Result Highlights

Hindalco Industries Ltd. has demonstrated a robust performance in Q2FY25, showcasing increased profitability, business expansion. Its revenue increased to Rs. 58,203 Crores showcasing 7% growth on Y-o-Y basis.

EBITDA grew to Rs. 9100 Crores in Q2FY25, showcasing a significant 49% Y-o-Y growth which shows improved profitability despite several segment challenges.

Profit After Tax (PAT) surged to Rs. 3,909 Crores, showcasing 78% increase Y-o-Y basis which is a positive indication for the company in terms of profitability.

Hindalco is planning to expand its capex which will involve an investment of $4-5 billion to increase its upstream capacity across two metals i.e., aluminium and copper. Funding will come from Internal accruals and debts amounting to Rs. 7200 Crores to Rs. 8,000 Crores, reflecting companies balanced and strategic move.

In addition to the above plans, Hindalco has already committed a massive investment of Rs. 6,000 Crores for increasing downstream capabilities and has also proceeding with $4.1 billion Bay Minette Project in the U.S. Hindalco is standing with a great vision and continuously focusing on several strategies to boost its revenue growth.

Hindalco Industries Ltd announced on Thursday that it has received a demand order worth around Rs 53 crore from the Odisha tax authority in a regulatory filing. The company revealed that the Central Goods and Services Tax (CGST) Commissioner in Rourkela has filed a claim under the Goods and Services Tax (GST) rules, which includes Rs 52.67 crore in fines and penalties.

The aluminum and copper manufacturing giant said The order was initially sent via after-hours email on Dec. 24, 2024. However, the company learned of the order on Thursday. After one employee quickly lost access to their official email account “As soon as we know the order. We will let you know,” Hindalko explained.

This demand relates to the GST payable by reverse surcharge on water bills paid to the state government. Hindalko plans to appeal the order. It asserts that there is a strong case on morality and law. The company emphasizes that it does not foresee any material impact to its financial, operating or other operations as a result of the order.

Hindalco announced strong financial performance for the quarter ended September 30, 2024, with net profit increasing 78% year-on-year to Rs 3,909 million. Revenue growth was driven by Strong performance in key business segments This includes Novelis, copper and aluminum operations. Notably, the aluminum upstream and downstream segments recorded revenue growth of 15% and 20%, respectively.

In the stock market, Hindalco shares closed marginally higher at ₹628.90 on BSE, underperforming the benchmark Sensex, which remained flat.

Stock Performance

Hindalco Industries Ltd.’s stock is currently trading at Rs. 617.40, it’s 52 weeks high has been 772.65- and 52-week low was 496.35 with market cap of 138,743 Crores. The fundamentals of the company look very strong there are no major reasons for the recent downfall. It’s the overall sentiment of the market trying the make a bearish trend. Stock is currently in the neutral range and a major accumulation is happening. The PE ratio is 10.64 and Price to Book Value 1.31, it denotes that company’s stock is not overvalued and trading in the fair range. It falls is good quality company basis long term financial performance.