UltraTech Cement Ltd., a flagship company of the Aditya Birla Group, is India’s largest manufacturer of grey cement, ready-mix concrete (RMC), and white cement. Established in 1983, the company has a strong presence across India, UAE, Bahrain, and Sri Lanka. UltraTech operates 23 integrated manufacturing units, 28 grinding units, and 7 bulk terminals, making it a leading player in the global cement industry. It has installed cement manufacturing capacity of approximately +140 million tonne per annum and has employee strength over 23000 in FY24. UltraTech is a pioneer in sustainability initiatives, with a focus on reducing carbon emissions, renewable energy adoption, and circular economy practices. It is committed to achieving carbon neutrality by 2050.

Return Summary

YTD

1 Month

6 Month

1 Year

2 Year

3 Year

5 Year

4.58%

-0.97%

7.91%

25.87%

59.37%

48.54%

155.7%

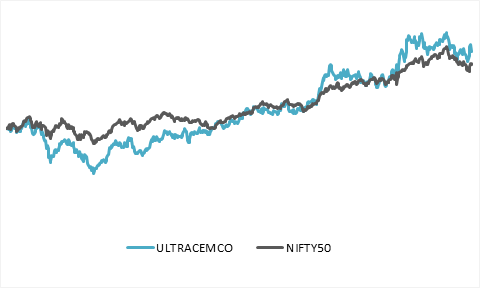

3 Year Return: UltraTech Cement v/s NIFTY

Result Highlights

Revenue of ₹15,635 in Q2 and EBITDA of ₹2017, which is multi quarter low because of monsoon season, election pressure and high cost compared to revenue.

UltraTech Cement’s capacity utilization at 68% with 3% growth in volume terms for Q2 FY25.

The high-cost fuel contracts are at end and by Q3 the prices will further go down and costs dropping to ₹1.84 per Kcal, down 8% QoQ.

Government focus on Metros, Roads, and Housing schemes will benefit cement companies.

The company will be expanding its capacity by 8 million tons reaching 158 million tons capacity.

The Kesoram Cement acquisition at ₹7500 crore, and it will strengthen and expand the south market footprint and will reach the target of total capacity of 200 million tons by 2028.

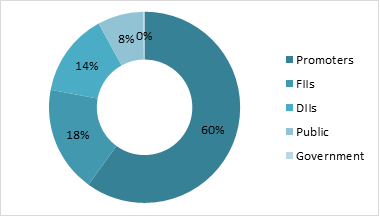

Shareholding Pattern

Return Comparison with Peers

COMPANY

1 Year

2 year

3 Year

5 Year

UltraTech Cement

26.03%

59.57%

48.72%

156.08%

Ambuja Cement

18.97%

(9.75%)

37.77%

150.30%

Shree Cement

(2.00%)

9.05%

(1.54%)

20.58%

JK Cements

16.05%

37.46%

27.79%

258.90%

JK Lakshmi Cements

(1.39%)

15.34%

23.17%

173.19%

Contribution to Industry Size

Being the largest cement company in Cement industry, UltraTech Cement with ₹318,000 crore market capitalizations having 24% market share of the industry. Expanding its footprint and having highest market share in North, South, West and East of India. Promoting the use of renewable energy resources for its production process and reducing the use of coal and pet coke. The company extensive operations include 23 integrated plants, 28 grinding units and 7 bulk terminals, enabling to serve the market efficiently.

Balance Sheet Analysis

Reserves, fixed assets and capex is increasing every year, showing a great sign of growth.

Company has debt on its balance sheet but has enough cash to pay it, hence it is net debt free.

The excess cash is used to acquire new business to have more growth through inorganic way as business is at mature stage to grow fast.

Cash Flow Analysis

Cash flow from Operations is ₹10,898 crore in FY24 and is positive for more than 10 years.

Purchase of fixed assets is in increasing trajectory every year on year, showing a great sign of expansion and growth of company.

The borrowing has been stable and is very low maintaining its debt to equity ratio.

India has earned the title of the “Pharmacy of the World” due to its unparalleled contributions to the global supply of affordable medicines, particularly during the COVID-19 pandemic. The country’s role in vaccine distribution and the production of essential drugs during this period has further cemented its reputation as the “Healers of the World.” These achievements highlight India’s critical role in addressing global healthcare needs by providing low-cost and high-quality medical solutions.

Current Industry Status

The Indian pharmaceutical industry, valued at $55 billion, is a key player in the global healthcare sector. It accounts for an impressive 20% of the world’s generic drug supply and fulfils 60% of the global vaccine demand, demonstrating its dominance in these areas. This success is attributed to India’s cost-effective manufacturing processes, skilled workforce, and strong infrastructure.

Future Projections

India’s pharmaceutical sector is set for remarkable growth, expected to reach $130 billion by 2030 and a staggering $1 trillion by 2047. This unprecedented expansion reflects the industry’s potential to transform into a global healthcare innovation hub. It will likely reinforce India’s leadership in drug discovery, manufacturing, and distribution, benefiting millions worldwide.

Global Growth Drivers

The following factors are driving India’s dominance in the pharmaceutical sector:

Low-Cost Manufacturing: India’s ability to produce high-quality drugs at lower costs makes it a preferred global supplier.

Growing Demand for Generics and Biopharmaceuticals: As healthcare costs rise worldwide, the demand for cost-efficient generic drugs and biosimilars is increasing.

Advanced Production Standards: Indian manufacturers adhere to strict quality protocols, earning trust in regulated markets like the US, Europe, and Japan.

Focus on Drug Innovation: India is actively advancing in biologics, innovative drug therapies, and active pharmaceutical ingredients (APIs).

Government Policies and Industry Initiatives

The Indian government is spearheading multiple initiatives to bolster the pharmaceutical industry:

PLI Schemes: Production Linked Incentives (PLI) are being provided to encourage domestic production of APIs and reduce dependency on imports from countries like China.

R&D Investments: Increased focus on research and development is helping India step into niche markets such as gene therapy and immunotherapy.

Industry Collaborations: Partnerships with global pharmaceutical companies are being encouraged to strengthen India’s competitive edge.

Impact on the Indian Stock Market

Sectoral Impact

The pharmaceutical sector is poised to see strong investor interest, with both domestic and international players looking to capitalize on the expected growth. The news is likely to create bullish momentum for pharmaceutical stocks, especially those focused on generics, vaccines, and biologics.

Key Beneficiaries

Major Companies: Sun Pharma, Dr. Reddy’s, Cipla, Biocon, Lupin, and Zydus Lifesciences are positioned to benefit significantly from this growth.

API Manufacturers: Companies like Divi’s Laboratories and Aarti Drugs are expected to gain as India moves towards greater self-reliance in API production.

Innovators: Firms investing in biosimilars, biologics, and cutting-edge research are likely to emerge as market leaders.

Long-Term Opportunities

The $1 trillion milestone by 2047 highlights the sector’s long-term potential, making it a compelling investment avenue for institutional and retail investors alikeBroader Implications for the Economy

Employment Generation: The pharmaceutical industry’s expansion will create millions of jobs across R&D, manufacturing, and logistics.

Boost to Exports: India’s export contribution is expected to grow significantly, further strengthening its foreign exchange reserves and global trade balance.

Healthcare Innovation Hub: With investments in biotechnology, clinical trials, and advanced drug discovery, India is on track to become a leading centre for healthcare innovation.

Conclusion

India’s pharmaceutical industry is entering a golden era, with projections of becoming a $1 trillion global leader by 2047. This growth not only cements India’s role as the pharmacy of the world but also creates vast opportunities for investment, innovation, and employment. By addressing both global and domestic healthcare needs, the sector is set to play a pivotal role in India’s economic and social development in the coming decades. Policymakers and investors must seize this moment to strengthen India’s infrastructure, innovation, and global partnerships, ensuring that the nation sustains its leadership in the pharmaceutical landscape.

Divi’s Laboratories Ltd., a major global API (Active Pharmaceutical Ingredients) manufacturer, was founded in 1990 as Divis Research Center, focusing initially on Research & Development. Today, it stands as one of the largest API companies worldwide, specializing in Intermediates, Nutraceuticals, and custom synthesis for innovator pharmaceuticals. It has a significant export-oriented business, with a presence in over 100 countries, supplying around 160 diverse products. Divi’s Laboratories Ltd. has achieved significant milestones in its growth and operations. In 1995, the company established its first manufacturing unit in Choutuppal near Hyderabad. Over the years 1997-2001, it earned ISO-9002 and OHSAS-18001 certifications, underlining its commitment to quality and safety standards. By 2002, Divi’s expanded further with a second manufacturing facility at Chippada, Visakhapatnam, which later became an Export Oriented Unit (EOU), enhancing global reach.

In 2006-2008, the company developed Divi’s Pharma SEZ in Visakhapatnam for Nutraceutical production, expanding its custom synthesis and Nutraceutical portfolio to meet rising export demand. In 2011, Divi’s launched the DSN SEZ Unit at Visakhapatnam, increasing production capacity in generic and custom synthesis segments.

From 2014-2018, Divi’s Laboratories passed multiple international regulatory inspections, including from the US FDA and COFEPRIS (Mexico), establishing EIR status for Unit-II, Visakhapatnam, which addressed previous regulatory concerns. The company invested ₹1200 crore in 2019-2020 in brownfield projects, creating DC SEZ and DCV SEZ units that became fully operational in FY2021. These projects boosted Divi’s role in generic and big pharma markets. In 2023, Divi’s launched Unit-III in Kakinada, Andhra Pradesh, further expanding production capacity.

In line with its dedication to innovation and compliance, Divi’s has research centers in Hyderabad and at manufacturing sites, focusing on custom synthesis and process innovations. With two subsidiaries—Divi’s Laboratories (USA) Inc. and Divi’s Laboratories Europe AG in Switzerland—the company enhances its reach in Nutra product markets. Divi’s continued investments in R&D, global regulatory compliance, and strategic expansion reinforce its commitment to high-quality pharmaceutical solutions, positioning it as a prominent player in the global API market.

Financial Overview

Industry Outlook

The Indian pharmaceutical sector is experiencing both near-term challenges and long-term growth potential driven by strategic expansions, cost efficiency, and new market opportunities. Key factors impacting the sector include pricing pressures in generic products and logistics challenges due to disruptions like the Red Sea crisis, which has extended shipping times and increased costs. Many companies are proactively managing inventory and supply chains to mitigate these impacts, such as advancing shipments and diversifying supply sources.

In the generic business, pricing pressure remains a challenge, but there is healthy volume growth in base businesses. Companies are expanding their portfolio to address loss of exclusivity (LOE) for several drugs, projected for 2026, which opens opportunities to capture market share in high-value molecules. This trend aligns with the pharmaceutical sector’s increasing focus on specialty and complex products and API (Active Pharmaceutical Ingredient) markets, which are seeing robust demand.

Custom synthesis continues to drive growth, with rising demand from both new and existing customers. Many companies have expanded into contrast media manufacturing, particularly iodine- and gadolinium-based molecules, which present a growing opportunity in global diagnostic markets with an annual growth rate of around 10-15%.

The API sector is well-positioned for sustained growth as global companies look for reliable alternative suppliers due to changing procurement strategies. With recent capacity expansions across SEZ units in India, companies can leverage low input costs in areas like raw materials, freight, and power to enhance profit margins. As inflation moderates globally, Indian pharmaceutical companies may also benefit from cost rationalization strategies, improving their competitiveness.

Divi’s Laboratories and other Indian firms are positioned to capitalize on the long-term trend of increased API demand and are exploring new opportunities in contract media and GLP-1 products. As the global addressable market for contrast media grows (estimated at USD 4-6 billion), firms expanding in this space can anticipate sustained demand for innovative and cost-effective solutions. Meanwhile, backward integration and advanced R&D capabilities are key strategies, enabling companies to streamline production costs and strengthen market positions over the long term.

In summary, while near-term challenges like pricing pressure and logistics disruptions persist, the pharmaceutical sector’s shift toward specialty products, cost-efficiency, and expanded capacities paints a promising outlook for the long-term. Indian companies’ strategic investments in innovation, compliance, and operational efficiency will likely enable them to maintain double-digit revenue growth while meeting the increasing demands of the global pharmaceutical market.

Business Segments

Divi’s Laboratories has demonstrated strong segmental performance across several key areas, including generic APIs, custom synthesis, peptides, contrast media, and ongoing capacity expansions at strategic units. Each of these segments reflects the company’s focus on meeting growing demand while managing industry challenges such as pricing pressures and supply chain disruptions.

Generic APIs: Divi’s generic business has experienced healthy double-digit volume growth, although pricing pressure persists across the industry. Despite the pricing environment, Divi’s has expanded its market share in smaller API molecules, highlighting the company’s resilience and strategic positioning in the generic segment. Emerging generic products have also shown robust performance, underscoring Divi’s adaptability in a competitive space.

Custom Synthesis: There is a notable increase in demand for Divi’s custom synthesis services from both new and existing clients. The future pipeline for this segment appears strong, with a robust set of products advancing through various stages of development. Key contributions from this segment are expected to start from FY26, aligning with the company’s long-term growth vision.

Peptides: Divi’s Laboratories has placed significant emphasis on GLP-1 compounds within the peptide segment, focusing on solid-phase synthesis to meet customer-specific requirements. The company is also expanding capacities for these peptide products, especially for solid-based peptides used in GLP-1 fragments, a growing therapeutic area. This focus enhances Divi’s specialty offerings, enabling it to cater to high-demand, niche markets.

Contrast Media: The contrast media segment has delivered impressive results, with volume growth of 20-30% YoY. Divi’s engagement with major clients in this area is progressing, with various projects moving to advanced stages. The company is actively working on iodine-based molecules (some nearing commercialization) and gadolinium-based molecules (in qualification stages, with potential for commercialization by FY26/27). Increased RFPs (Request for Proposals) from customers in this segment underscore the growing demand for Divi’s contrast media products.

Kakinada Unit (Unit-III): Divi’s Greenfield expansion at Kakinada is progressing as planned, with Rs. 11.8 billion spent as of H1 FY25. Production is set to commence in December 2024 in a phased manner. This unit is part of Divi’s strategy to expand capacity for both regulatory and custom synthesis products, supporting future growth in demand.

Logistics and Supply Chain: Divi’s has been proactive in managing inventory and logistics challenges, particularly those arising from the Red Sea disruptions that increased transit times to 70 days. The company has addressed these challenges by advancing shipments by 3-4 weeks and maintaining higher safety stock to minimize supply interruptions.

Key Subsidiaries and Their Information

Divi’s Laboratories operates through two major subsidiaries, Divis Laboratories (USA) Inc. and Divi’s Laboratories Europe AG. These subsidiaries play a strategic role in the company’s global expansion and focus on specialized markets for pharmaceutical ingredients, particularly in custom synthesis and nutraceuticals.

Divis Laboratories (USA) Inc.: This subsidiary caters primarily to the North American market, focusing on the distribution and marketing of nutraceutical products and custom synthesis services. It helps Divi’s Laboratories establish a strong presence in the US, one of the largest pharmaceutical markets globally, and aligns with Divi’s mission to support local customer requirements while meeting stringent regulatory standards. It contributes significantly to the company’s nutraceutical portfolio growth and has enhanced relationships with major pharmaceutical clients by providing reliable supply chains and custom synthesis offerings tailored to local industry needs.

Divi’s Laboratories Europe AG (Switzerland): This subsidiary focuses on European markets, providing nutraceutical and pharmaceutical ingredients and supporting custom synthesis projects for clients in Europe. Divi’s Laboratories Europe AG serves as a critical hub for European operations and facilitates compliance with EU regulatory standards. It also strengthens Divi’s supply chain resilience by creating a local presence in Europe, enhancing service delivery and customer support. In FY25, Divi’s Laboratories Europe AG has seen robust demand in nutraceuticals, particularly for ingredients with high-quality standards essential for the European market. This subsidiary plays a key role in Divi’s market penetration in Europe, contributing to the company’s overall revenue growth.

These subsidiaries support Divi’s Laboratories’ strategic goals of expanding its global footprint and catering to diverse regional needs in the pharmaceutical and nutraceutical industries. They also provide a platform for Divi’s to directly engage with key markets, ensuring regulatory compliance, effective supply chains, and tailored customer support, aligning with the company’s vision of global operational excellence.

Q2 FY25 Highlights

Divi’s Laboratories reported consolidated total income of ₹2,444 crore, a 22.5% increase compared to ₹1,995 crore in the same quarter of the previous year. For the half-year ended 30th September 2024, Divi’s Laboratories posted a consolidated total income of ₹4,640 crore, up by 20.4% from ₹3,854 crore in the same period of the previous year. This consistent revenue growth reflects the company’s ability to expand its product portfolio and global footprint.

Profit Before Tax (PBT) for the quarter was ₹722 crore, a substantial rise of 54% from ₹469 crore in the corresponding period last year. This increase in PBT highlights improved profitability driven by efficient operations and cost management. The PBT for the half-year was ₹1,326 crore, up from ₹961 crore, marking a 38% increase.

Profit After Tax (PAT) for the quarter stood at ₹510 crore, showing a significant 46.6% growth compared to ₹348 crore in the previous year. This reflects the company’s strong bottom-line performance, driven by both operational growth and improved cost efficiencies. PAT for the half-year was ₹940 crore, a significant 33.5% increase from ₹704 crore in the corresponding period of the previous year, reflecting robust operational performance and better margins.

The company also reported a foreign exchange (forex) gain of ₹29 crore for the quarter, which is a notable increase from the ₹1 crore gain recorded in the same quarter of the previous year. The company also recorded a forex gain of ₹28 crore for the half-year, compared to ₹14 crore in the previous year, further contributing to the positive financial results. The forex gain likely provided additional support to the bottom line.

Greenfield expansion at Kakinada Unit(III) is progressing as planned, with Rs. 11.8 billion spent as of H1 FY25. Production is set to commence in December 2024 in a phased manner. This unit is part of Divi’s strategy to expand capacity for both regulatory and custom synthesis products, supporting future growth in demand.

Divi’s has been proactive in managing inventory and logistics challenges, particularly those arising from the Red Sea disruptions that increased transit times to 70 days. The company has addressed these challenges by advancing shipments by 3-4 weeks and maintaining higher safety stock to minimize supply interruptions.

Financial Summary

INR in Cr.

Q2FY25

Q1FY25

Q2FY24

Q-o-Q (%)

Y-o-Y (%)

Revenue from Operation

2,338

2,118

1,909

10%

22%

Other Income

106

79

86

34%

23%

Total Income

2,444

2,197

1,995

11%

23%

Total Expenditure

1,622

1,496

1,430

8%

13%

Operating profit

716

622

479

15%

49%

Other Income

106

79

86

34%

23%

Interest

1

0

1

0%

0%

Depreciation

99

97

95

2%

4%

PBT

722

604

469

20%

54%

PAT

510

430

348

19%

47%

EPS (Rs.)

19.2

16.2

13.11

19%

46%

SWOT Analysis: Key Insights

Strengths

Market Leadership: Strong foothold in the industry with a leading market position.

Robust Manufacturing: Advanced manufacturing capabilities that ensure high-quality production.

Research Focus: Commitment to R&D fuels innovation and keeps the company competitive.

Outstanding Performance: Consistently strong financial and operational performance.

Weaknesses

Regulatory Risks: Exposure to regulatory changes can impact business operations.

High Dependency on API: Reliance on active pharmaceutical ingredients (API) poses risks.

Limited International Reach: Lack of significant presence in global markets limits growth potential.

Opportunities

Rising Global Demand: Increasing demand for pharmaceutical products worldwide.

New Product Development: Expanding product lines can capture new market segments.

Technological Innovations: Leveraging technology to enhance production and product quality.

Threats

Price Pressure: Competitive pricing in the market can impact profit margins.

Intense Competition: Facing stiff competition from both domestic and international players.

Supply Chain Vulnerabilities: Disruptions in the supply chain could affect operations.

The Patanjali Group, founded by Baba Ramdev and Acharya Balkrishna, is a prominent Indian conglomerate known for its focus on natural, Ayurvedic, and wellness-oriented products. Initially centered on Ayurveda and herbal health, the group rapidly expanded into diverse sectors, including FMCG, healthcare, food products, personal care, and education. Key brands like Patanjali Ayurved and Patanjali Foods offer a wide range of products, from food items and supplements to cosmetics and home care products. With a mission to promote traditional Indian medicine and healthy living, the Patanjali Group has become a household name, emphasizing quality, affordability, and a focus on sustainable practices. Incorporated in 1986, Patanjali Foods Limited is a leading FMCG company in India, known for its presence across edible oils, food & FMCG, and wind power generation sectors. Originally known as Ruchi Soya Industries Limited, the company has established a strong portfolio of brands, including Patanjali, Ruchi Gold, and Nutrela, offering products at various price points to meet diverse consumer needs. Patanjali Foods is engaged in processing oil seeds, refining crude oil, and producing a variety of food products, such as biscuits and nutraceuticals. It also has a significant focus on renewable energy with wind power generation operations and maintains an extensive network of manufacturing plants across India.

Industry Outlook

For FY25, the industry outlook for Patanjali Foods appears promising, driven by growth in the FMCG and health foods sectors, a rising demand for natural and organic products, and increasing health consciousness among Indian consumers. The edible oil segment, a major contributor to Patanjali Foods’ revenue, is expected to grow due to increased consumption and demand for healthier oil alternatives. The health and wellness segment, particularly nutraceuticals, is also gaining momentum as consumers prioritize immunity and preventive health.

According to recent market reports, the FMCG sector in India is projected to grow at a compound annual growth rate (CAGR) of around 12-14% through 2025. The edible oils market, specifically, may see a CAGR of 9-10%, while the nutraceutical segment, where Patanjali Foods is expanding, is estimated to grow at a CAGR of 15-17%.

These growth rates align with Patanjali Foods’ strategy to diversify its product portfolio and increase its market share across segments. With its focus on affordable, natural, and Ayurvedic products, Patanjali Foods is well-positioned to benefit from these industry trends in FY25.

Business Segments

Patanjali Foods operates in two main business segments: Edible Oils and Food

& FMCG.

Edible Oils: This segment is the largest contributor, accounting for

approximately three-fourths of Patanjali Foods’ total revenue. In Q2 FY25,

the Edible Oils segment experienced a 10% increase in revenue, reaching

₹5,939 crore, largely supported by stable demand. Branded edible oils played

a significant role, contributing nearly 74% to this segment’s revenue. This

steady demand helped drive the overall revenue for the company to

₹8,154 crore for the quarter, reflecting an overall growth of about 4%

compared to the previous year.

Food & FMCG: The Food and FMCG segment, though smaller, accounted for around 25% of the total revenue in Q2 FY25. However, the segment faced challenges, with a 7% decline in revenue, attributed to sluggish demand in the broader industry. Despite this, staples like rice, pulses, and wheat performed better, with sales reaching ₹1,032 crore. The segment’s EBITDA for Q2 FY25 was ₹234 crore, reflecting some impact from the softer demand for other FMCG products.

Wind power generation: Although smaller in scale, this segment generated revenue of ₹14 crore, showcasing Patanjali Foods’ commitment to sustainable energy by fulfilling 20% of its energy needs through renewable sources.

Key Subsidiaries and Their Information

Patanjali Foods Limited has several key subsidiaries that enhance its operations and product offerings, particularly in the FMCG sector and edible oils. Here are the main subsidiaries as of FY25:

Ruchi Soya Industries Limited: This is one of the largest subsidiaries, focusing on edible oils and food products. It significantly contributes to Patanjali Foods’ revenue through its various brands, including Ruchi Gold and Nutrela. Following its acquisition by Patanjali in 2021, Ruchi Soya has been integral to the company’s operations.

Patanjali Ayurved Limited: This subsidiary plays a crucial role in providing a range of Ayurvedic and herbal products. Patanjali Foods has expanded its FMCG offerings by acquiring the food business from Patanjali Ayurved, which includes a variety of consumer-focused products.

Patanjali Natural Biscuits Private Limited: This subsidiary is involved in the production of biscuits and snacks, further diversifying Patanjali’s product range in the FMCG sector.

Patanjali Wind Energy Private Limited: Engaged in wind power generation, this subsidiary contributes to the company’s sustainability efforts by utilizing renewable energy sources. In Q2 FY25, it generated revenue of ₹14 crore from this segment.

Q2 FY25 Highlights

In Q2 FY25, Patanjali Foods Limited reported robust performance despite a challenging environment in both the Food & FMCG and Edible Oils segments. The company’s revenue from operations reached ₹8,154.19 crore, marking a 4.25% year-on-year (YoY) growth.

Patanjali Foods achieved its highest-ever EBITDA of ₹493.86 crore, reflecting a 17.81% YoY improvement. The EBITDA margin also expanded by 70 basis points to 6.06%.

Gross profit rose significantly from ₹1,021.26 crore to ₹1,292.81 crore, primarily due to favorable pricing scenarios in the market. The PAT increased by 21.38% YoY to ₹308.97 crore, with a corresponding margin improvement of 53 basis points.

There has been a noticeable shift in consumer preferences from traditional General Trade channels to modern trade, e-commerce, and quick commerce, leading to higher inventory levels among traditional partners. The company exported products to 21 countries, generating ₹34.55 crore in revenue from exports during the quarter.

The wind turbine power generation segment contributed ₹14.35 crore in revenue, with the company sourcing approximately 20% of its energy needs from renewable sources.

During the quarter, Patanjali Foods significantly increased its advertising and sales promotion expenses, surpassing ₹130 crore, which brought the total for H1 FY25 to over ₹185 crore. The company launched various marketing campaigns across print, social media, TV, and radio, promoting specific products. Notably, celebrities such as Shilpa Shetty, Shahid Kapoor, and Khesari Lal Yadav were engaged to endorse Nutrela-branded soya chunks, edible oils, and nutraceuticals, respectively.

In addition to celebrity endorsements, Patanjali initiated the Rural Connect Program and Nutrela Operation Thunder to enhance brand visibility and distribution in rural, underserved markets. The brand also collaborated with popular YouTube channels like Rajshri Foods and Get Curried, featuring star chefs who showcased enticing recipes using Nutrela product.

Financial Summary

INR in Cr.

Q2 FY25

Q1FY25

Q2FY24

Q-o-Q Growth

Y-o-Y Growth

Total Revenue

8154

7173

7822

13.68%

4.25%

Selling/ General/ Admin Expenses Total

130

117

91

10.94%

43.59%

Depreciation/ Amortization

56

57

60

-0.90%

-6.07%

Total Operating Expense

7762

6824

7487

13.73%

3.67%

Operating Income

393

349

335

12.63%

17.15%

Profit Before Tax

417

359

335

16.13%

24.42%

Profit After Tax

309

263

255

17.46%

21.23%

Diluted Normalized EPS

8.53

7.26

7.03

17.49%

21.34%

SWOT Analysis

Strengths:

Wide range of products

Strong brand reputation

Extensive reach in both rural and urban areas

Solid financial performance

Weaknesses:

Heavy reliance on edible oils

Limited international presence

High costs of raw materials

Opportunities:

Rising consumer interest in health and wellness products

Growth in online and modern retail channels

Potential to expand into underserved rural markets

L&T Finance Holdings, part of the Larsen & Toubro Group, is a key player in India’s financial sector, offering a wide range of services across rural, housing, and infrastructure finance. Through its subsidiaries, it provides products like microfinance, two-wheeler loans, farm equipment finance, and home loans. The company is also involved in financing large-scale infrastructure projects.

L &T Finance emphasizes digital transformation, using data analytics and AI to enhance customer experience and streamline operations. It has adopted a strong Environmental, Social, and Governance (ESG) framework, ensuring sustainable business practices. In recent years, it has improved asset quality by reducing non-performing assets (NPAs) and focusing on cost optimization. With a focus on retail and rural finance, L&T Finance is committed to long-term, responsible growth in India’s financial ecosystem.

Industry Outlook

India’s economy is projected to grow by 7% in FY25, driven by strong private consumption and credit demand. This growth is set to significantly boost the financial sector, particularly non-bank financial companies (NBFCs), which are expected to see increased profitability despite higher funding costs. Credit demand is likely to expand, especially in infrastructure, housing, and microfinance sectors, with NBFC loan growth projected to increase by 15%, fueled by strong performance in key consumption areas. Infrastructure lending is poised for substantial growth due to large investments in energy and urban development. L&T Finance plans to expand its infrastructure portfolio by over 20% to capitalize on these opportunities. Additionally, the company is focused on improving asset quality, aiming to reduce its Gross Non-Performing Assets (NPAs) to below 3.0%, down from 3.1% in FY24. L&T Finance is also expected to enhance its sustainability efforts by increasing its allocation towards ESG projects.

Business Segments

Rural Finance: This includes microfinance, farm equipment finance, and two-wheeler loans, primarily catering to rural consumers. It plays a key role in driving financial inclusion in India’s rural economy.

Retail Finance: L&T Finance offers home loans, loans against property, and other personal loans, targeting individual consumers in urban and semi-urban areas.

Infrastructure Finance: The company has a significant presence in financing large-scale infrastructure projects, such as energy, transportation, and urban development, supporting India’s infrastructure growth.

Mutual Funds and Wealth Management: Through L&T Investment Management, the company manages a wide range of mutual funds and wealth management products for retail and institutional investors.

Q2 FY25 Highlights

L&T Finance reported a Profit After Tax (PAT) of ₹696 crore, reflecting a 17% increase compared to the previous year. This growth is a strong indicator of the company’s profitability and overall financial health.

The company maintained a stable Return on Assets (RoA) at 2.60%, up 18 basis points year-over-year. With 96% of its loan book now in retail financing, it is advancing its “retailization” strategy to reduce corporate loan dependence and improve asset quality.

L&T Finance’s retail loan portfolio grew 28% YoY to ₹88,975 crore, driven by strong demand for home loans, vehicle financing, and microfinance. The consolidated book grew 18% YoY, the highest since Q1FY20.

L&T Finance improved its Net Interest Margin (NIM) to 8.94%, up by 32 bps YoY, while reducing its Weighted Average Cost of Borrowings (WACB) to 7.80%, down by 5 bps. Credit cost remained stable at 2.59%, and the collection efficiency for the rural segment stood at 99.45%.

Company Overview Just Dial Ltd., founded on December 20, 1993, in Mumbai, India, is led by CEO Venkatachalam Sthanu Mani. As a key player in the Technology Services sector, particularly in Internet Software/Services, Just Dial is a leading local search engine in India. It offers comprehensive search services via website, mobile app, phone, and SMS, helping users find businesses, products, and services.

The latest JD App integrates features like Map-aided Search, Live TV, and Stock Quotes, making daily tasks easier. Just Dial also provides services such as bill payments and travel bookings, generating revenue through search services, transaction commissions, and certifications.

The Internet Software and Services industry is growing rapidly due to increased internet use, digital transformation, and the shift to online platforms. Companies like Just Dial are well-positioned as more people rely on digital tools to find local businesses and services. The industry is being reshaped by emerging technologies like AI and automation, enhancing user experiences and operational efficiency. With a focus on mobile apps and personalized solutions, businesses are catering to the rising smartphone user base. As digital adoption spreads, especially in rural areas, localized search services are expected to thrive, driving further growth and innovation in the industry.

Business Segments:

Local Search Services: Users can discover businesses, products, and services via website, app, and SMS.

Transaction Services: Includes bill payments, travel bookings, and online transactions.

Rating Certifications: Business rating and certification services.

Website Creation & Digital Marketing: Offers website building and marketing solutions.

Revenue Streams: Search-related services, service certifications, and transaction commissions.

Earnings Report:

Q1 Results:

Net Profit: ₹141 crore

Revenue: ₹281 crore

Operating Expenses: ₹214 crore

Profit Before Tax (PBT): ₹154 crore

Q2 Results:

Net Profit: ₹154 crore (9% increase from Q1)

Revenue: ₹285 crore

Operating Expenses: ₹217 crore

Profit Before Tax (PBT): ₹182 crore

Summary: Strong financial performance with growth in net profit and revenue from Q1 to Q2.

Financial Summary

Just Dial’s financial performance has shown significant growth over the recent quarters. In Q1, the company achieved a net profit of ₹141 crore with revenue of ₹281 crore, accompanied by operating expenses of ₹214 crore and a Profit Before Tax (PBT) of ₹154 crore.

By Q2, Just Dial reported a net profit of ₹154 crore, marking a 9% increase from the previous quarter. Revenue rose to ₹285 crore, with operating expenses slightly higher at ₹217 crore. The PBT for Q2 reached ₹182 crore, reflecting the company’s robust financial health and effective cost management strategies.

Performance Overview:

Just Dial Ltd. delivered a strong performance in Q2 FY25, with significant growth across key financial metrics. The company’s net profit surged by 114% year-over-year, reaching ₹154 crore, driven by efficient cost management and rising revenue. Revenue from operations grew by 9%, totaling ₹285 crore, reflecting sustained demand for its digital solutions. The company also reported a 25% increase in total income and a 98% rise in profit before tax, signaling robust profitability. With strategic investments in technology and a growing user base, Just Dial continues to strengthen its position in the market.

Debt and Coverage:

Just Dial Ltd. maintains a healthy financial position with manageable debt levels.

Debt: ₹2.80B (2023), up from ₹700M (2020)

Free Cash Flow: ₹64B

Cash Reserves: ₹48B

Strong debt coverage ensures financial stability and growth.

Stock Performance: Just Dial’s stock has shown impressive growth, with a 2.96% increase on the BSE to ₹1,307.10 after its Q2 FY25 report and a 7% surge on the NSE to ₹1,359. Over the past year, the stock delivered a 76.10% return, with a 5-year growth of 110.43%. Its market cap stands at ₹100.10 billion, reflecting investor confidence.

SWOT Analysis: Strengths: Strong brand, profit growth, AI investments. Weaknesses: Limited global presence, rising debt. Opportunities: B2B expansion, AI integration. Threats: Intense competition, market dependency.

Conclusion:

In conclusion, Just Dial Ltd.’s Q2 FY25 performance highlights its strong market position and effective cost management, evidenced by significant profit and revenue growth. With strategic investments in technology and a focus on B2B expansion, Just Dial is well-positioned for continued success and value creation for stakeholders.