HDFC Bank Q3 FY25 Earnings: Strong Deposit Growth, AUM Expansion, and Profit Surge Across Key Metrics

HDFC Bank Ltd: Overview

HDFC Bank Ltd., one of India’s leading private sector banks, was incorporated in 1994 and is headquartered in Mumbai. Renowned for its robust operational efficiency and customer-centric approach, the bank offers a diverse range of banking and financial services, including retail banking, wholesale banking, treasury operations, and digital banking solutions. HDFC Bank has established itself as a market leader in the Indian financial sector with its innovative approach, strong risk management framework, and expansive reach. With a network of over 7,000 branches and 19,000 ATMs across urban, semi-urban, and rural areas, the bank ensures accessibility to financial services for millions of customers.

Its commitment to digitization and innovation has made it a pioneer in offering cutting-edge digital banking products and services. The Indian banking industry is experiencing steady growth, driven by increased digital adoption, rising credit demand and the government’s focus on financial inclusion. HDFC Bank is well-positioned to leverage these opportunities due to its strong brand equity, extensive distribution network, and strategic focus on retail lending and digital transformation.

Latest Stock News

HDFC Bank reported strong performance across key metrics. Deposits saw a significant year-on-year (YoY) growth, with average deposits increasing by ₹3.36 trillion (15.9%) and end-of-period (EOP) deposits rising by ₹3.50 trillion (15.8%). The bank’s assets under management (AUM) also witnessed growth, with average AUM increasing by ₹1.86 trillion (7.6%) and EOP AUM up by ₹1.55 trillion (6.1%). The gross non-performing asset (NPA) ratio stood at 1.42%; with non-agriculture gross NPA at 1.19%. Liquidity coverage improved significantly, reaching 125% in December, compared to 110% in the previous year.

HDB Financial Services added 0.9 million customers and 20 branches during Q3 FY25, with its loan book growing to ₹1,021 billion, marking a 22% YoY increase and a 4% sequential rise. HDFC Life Insurance sold 294,000 individual policies during the quarter, a 2% increase from the previous year, insuring 11 million lives overall. It recorded a New Business Premium of ₹79 billion with a new business margin of 26%. HDFC Asset Management Company reported 12.6 million unique investors and achieved a 24% penetration in the mutual fund industry, strengthening its leadership position.

Business Segments

- Wholesale Banking: The Wholesale Banking Business of HDFC Bank serves a diverse clientele including Large Corporates, Multinational Corporations, Government, Public Sector Enterprises, Emerging Corporates and Business Banking/SMEs. Offering a wide array of financial products and services such as loans, deposits, payments, collections, tax solutions, trade finance, cash management solutions and corporate cards, etc. This business largely covers the rental discounting business as well as construction finance.

- Retail Banking: HDFC Bank’s Retail Business caters to a varied client base which includes Individuals, salaried professionals, small businesses like kirana stores, and Non-Resident Indians (NRIs). Among the offerings are Savings and Current Accounts, various loan options for personal and business needs, Credit and Debit Cards, Digital Wallets, Insurance and Investment Products and Remittance Services.

- Treasury: The Treasury department is responsible for managing the Bank’s liquidity requirements, as well as handling its investments in securities and other market instruments. It manages the balance sheet’s liquidity and interest rate risks and ensures compliance with statutory reserve requirements. It also manages the treasury needs of customers and earns a fee income generated from transactions customers undertake with your Bank, while managing their foreign exchange and interest rate risks.

- Digital & Payments Business: HDFC Bank is at the forefront of India’s digital banking revolution, offering a range of mobile and internet banking services. It is a leader in payment solutions, including credit and debit cards, point-of-sale terminals, and payment gateways. The bank’s “Digital 2.0” initiative focuses on enhancing customer experience through AI, machine learning, and automation.

Subsidiary Information

- HDFC Securities Ltd: HDFC Securities Ltd. is one of India’s leading stockbroking companies, renowned for its comprehensive range of investment and financial services. It offers products across various categories, including equity trading, mutual funds, fixed-income products, insurance, and investment advisory services. The company serves retail and institutional clients, ensuring accessibility through both online platforms and an extensive network of physical branches.

- HDB Financial Services Ltd: HDB Financial Services Ltd. is a non-banking financial company (NBFC) under HDFC Bank that specializes in providing innovative and customized financing solutions. Its product portfolio includes personal loans, business loans, gold loans, and consumer durable loans, catering to individuals, small businesses, and enterprises.

- HDFC AMC Ltd: Although HDFC Asset Management Company Ltd. (HDFC AMC) is no longer a direct subsidiary post-merger with HDFC Ltd., it continues to maintain close synergies with HDFC Bank. HDFC AMC is one of India’s largest mutual fund houses, providing a diverse range of investment solutions across equity, debt, and hybrid funds.

- HDFC Ergo General Insurance Company Ltd: HDFC Ergo General Insurance Company Ltd. is a joint venture between HDFC Ltd. and Ergo International AG, offering a comprehensive suite of general insurance products. Its portfolio includes health insurance, motor insurance, travel insurance, home insurance, and commercial insurance solutions.

- HDFC Pension Management Company Ltd: HDFC Pension Management Company Ltd. is a key player in India’s retirement planning ecosystem. As a pension fund manager under the National Pension System (NPS), the company helps individuals secure their post-retirement financial future.

Q3 FY25 Earnings

- Revenue of ₹85040 crore in Q3 FY25 up by 9.01% YoY from ₹78008 crore in Q3 FY24.

- Financing Profit of ₹-3181 crore in this quarter at a margin of -4% compared to -20% in Q3 FY24.

- Profit of ₹18340 crore in this quarter compared to a ₹17718 crore profit in Q3 FY24.

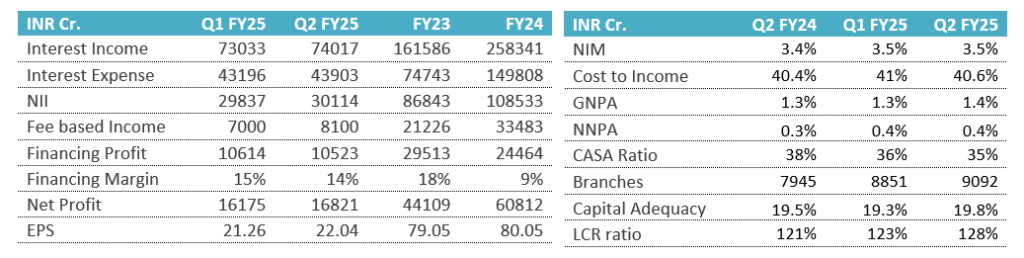

Financial Summary

| Amount in ₹ Cr | Q3 FY24 | Q3 FY25 | FY23 | FY24 |

| Revenue | 78008 | 85040 | 170754 | 283649 |

| Interest | 43242 | 46914 | 77780 | 154139 |

| Expenses | 50530 | 41307 | 63042 | 174196 |

| Financing Profit | -15764 | -3181 | 29932 | -44685 |

| Financing Margin | -20% | -4% | 18% | -16% |

| Other Income | 37007 | 27154 | 33912 | 124346 |

| Net Profit | 17718 | 18340 | 46149 | 65446 |

| NPM | 22.7% | 21.6% | 27% | 23.1% |

| EPS | 22.7 | 23.1 | 82.4 | 84.3 |