JB Chemicals & Pharma Shares in Spotlight as KKR Plans to Offload 10.2% Stake

Business and Industry Overview:

J B Chemicals and Pharmaceuticals Ltd (JBCPL) is a leading Indian medicine company. It has been making quality medicines for 47 years. It is one of the top 25 pharmaceutical companies in India. The company makes 350+ medicines for 20+ health problems. These include heart diseases, stomach issues, infections, and pain relief. Some of its famous brands are Rantac (for acidity), Metrogyl (for infections), and Nicardia (for high blood pressure). JBCPL has 5000+ employees. They work in 10 offices across India. JBCPL has 8 modern factories in India. These factories follow strict quality rules set by global health agencies. One of these factories is specialised in making lozenges (medicated throat candies). The company also sells medicines in over 40 countries. Some of its biggest markets are Russia, South Africa, and the U.S. In the last three years, JBCPL has been the fastest-growing pharma company in India. It has grown by launching new medicines, acquiring other brands, and expanding into new countries. The company has a strong financial position. It invests in research, technology, and high-quality production. JBCPL continues to grow and improve healthcare in India and around the world.

The pharmaceutical industry makes medicines that treat diseases and help people live healthier lives. This industry is growing fast because healthcare needs are increasing. New technology helps companies develop better medicines for different diseases. India is a major player in the global pharmaceutical industry. It is known as the “Pharmacy of the World” because it makes high-quality medicines at affordable prices. India is the world’s largest supplier of generic medicines. Generic medicines are cheaper versions of branded medicines, but work the same. India also produces low-cost vaccines that are used in many countries. One of India’s greatest achievements is providing affordable HIV treatment. This has saved many lives worldwide. India also makes affordable vaccines that help protect people from diseases. Because of this, India is important in global healthcare. India’s pharmaceutical industry is strong because of low manufacturing costs. It costs 30% to 35% less to make medicines in India compared to the US and Europe. Research and development (R&D) costs are also much lower in India—87% less than in developed countries. This helps make medicines affordable for more people. The country has many skilled workers, but their salaries are lower than in other countries, which keeps production costs down. The Indian pharmaceutical market is growing. By 2030, it is expected to be worth $130 billion. By 2047, it could reach $450 billion. The government is helping by providing support to increase production and attract investment. One of the ways it helps is through the Production-Linked Incentive (PLI) scheme. This scheme encourages companies to produce more medicines and create more jobs. The government also helps small pharma companies improve their products through the Strengthening of Pharmaceutical Industry (SPI) Scheme. India makes it easy for foreign companies to invest in the pharmaceutical sector. India allows 100% foreign investment in new pharma projects. Since 2000, India has received $22 billion in foreign investments for pharmaceuticals. This shows that foreign companies trust India’s pharma industry. India’s pharmaceutical companies sell medicines to many countries, including the US and Europe. India has the largest number of USFDA-approved factories outside the US. It also has over 2,000 WHO-GMP-approved factories, meaning the medicines made in India meet high international standards. With the help of the government, low costs, and new technology, India’s pharmaceutical industry will continue to grow and provide affordable medicines to people all around the world.

JB Chemicals and Pharma Ltd. is a leading company in the medicine industry. It makes a wide variety of medicines for different health problems. The company has modern factories in India. These factories meet international standards, which ensure the quality of their medicines. JB Chemicals sells its products in more than 40 countries. Some of the biggest markets include the US and South Africa. The company can keep production costs low. This allows it to offer high-quality medicines at affordable prices. JB Chemicals focuses on creating new medicines. It also works on improving its existing products. This helps the company stay ahead in the market. The company has strong business partnerships. These partnerships help JB Chemicals reach more customers and grow faster. JB Chemicals is known for its reliable healthcare products. People trust the company for its quality and consistency. The company is growing quickly in both India and abroad. It continues to make medicines that help people live healthier lives.

Latest Stock News:

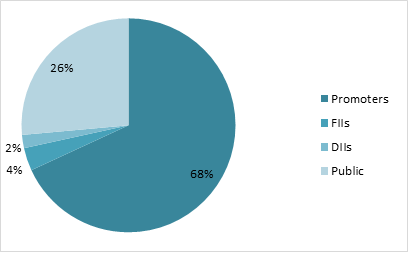

Tau Investment Holdings, a company connected to KKR, sold shares of JB Pharma. They sold 89.83 lakh shares, which is 5.78% of the company. Before selling, they owned 53.66% of JB Pharma. After the sale, their ownership dropped to 47.88%. The shares were sold for ₹1,625 each. This price was slightly lower than the previous day’s price. Even after selling the shares, Tau Investment Holdings still holds a big part of the company. JB Pharma gave 1,700 new shares to employees. These employees had been given stock options as a benefit from the company. They were able to buy these shares at a price. The company received ₹13,32,500 from this process. As a result, the total number of shares in the company increased from 15,56,75,508 to 15,56,77,208. JB Pharma’s manufacturing facility in Gujarat was inspected by the USFDA (U.S. Food and Drug Administration). The inspection took place from March 10 to March 13, 2025. After the inspection, the USFDA found no issues. This means the company is meeting all the required standards for making its products. JB Pharma received a great score for its work on sustainability. The Dow Jones Sustainability Index (DJSI) gave the company a score of 77. The DJSI is a list of the world’s top companies for sustainability. This score shows that JB Pharma is among the best in India and the world for its efforts on the environment and social responsibility. The company has worked on many projects, such as using renewable energy, saving water, reducing waste, and supporting communities. These actions helped JB Pharma earn this high score.

In summary, JB Pharma is doing well in business. The company is following good quality standards, and it cares about the environment and society. They are also helping their employees and making sure their manufacturing facilities meet the highest standards.

Potentials:

JB Pharma wants to become a leader in the medical industry. They plan to make new medicines and improve the ones they already have. The company is focusing on expanding its market reach and selling more products worldwide. They are working hard to grow in international markets. Currently, they are strong in Russia, South Africa, and the United States. They want to expand further into these regions and other places like Europe, Southeast Asia, the Middle East, and Brazil. This will allow more people to use their products. The company is also investing in new factories. They plan to build modern factories to meet the increasing demand for their medicines. They will also upgrade the ones they already have. This will help them keep the quality of their products high. JB Pharma cares about the environment and society. They are working to reduce their impact on the environment by using renewable energy and reducing waste. The company is also focused on helping local communities and being responsible in its operations. In the next two years, JB Pharma plans to increase its revenue by 12-14%. They want to achieve this by growing their chronic medicine products and their contract manufacturing business. This will help the company become more profitable. Each year, JB Pharma plans to launch 6 to 8 new products in India. Some of these products include an iron syrup and a dental probiotic. These products are expected to bring in a lot of revenue for the company. The company also wants to grow its contract manufacturing business. JB Pharma plans to double its revenue from this business in the next 3 to 5 years. They are already one of the top manufacturers of lozenges and sell them in over 40 countries. Additionally, JB Pharma is looking to buy other companies in different areas of healthcare, like heart care, eye care, children’s health, and digestive health. They recently bought some eye care products from Novartis, which will help them expand in this field. JB Pharma is committed to sustainability. They have reduced their energy use by 9% and are now using renewable energy in their operations. The company will continue to focus on sustainability in the future. Overall, JB Pharma’s plans focus on growing their market, improving their products, and being a responsible company that cares for the environment and society.

Analyst Insights:

- Market capitalisation: ₹ 25,352 Cr.

- Current Price: ₹ 1,628

- 52-Week High/Low: ₹ 2,030 / 1,434

- Stock P/E: 39.6

- Dividend Yield: 0.75%

- Return on Capital Employed (ROCE): 24.6%

- Return on Equity (ROE): 20.0%

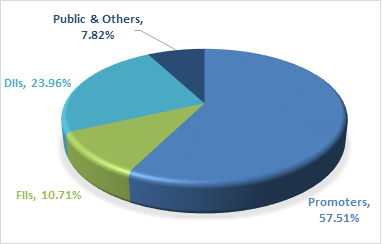

J.B. Chemicals & Pharmaceuticals Ltd (JBCPL) is a strong company that has been growing well. In the last year, its sales and profits grew by 25%. This means the company is doing better and earning more money. The company makes good profits. It has a profit margin of 26%, which shows it is good at keeping costs low and making money. This is a good sign. JBCPL also gives good returns to investors. It has a return on equity (ROE) of 20%. This means the company is using its money well to make profits. It also gives a good return on capital, which shows it is managing its money smartly. The company has low debt. This is important because it means the company does not owe a lot of money. Low debt makes the company safer and more stable. JBCPL earns money in different ways. 55% of its income comes from selling products in India, while 30% comes from selling products in other countries. It also earns 13% from making products for other companies. This helps the company stay stable. The company pays a small dividend to its investors. Even though the stock is priced higher than its book value, JBCPL’s growth and strong financial health make it a good investment. To sum up, JBCPL is a good company to invest in. It has strong profits, low debt, and is growing well. It is a safe and stable choice for people who want steady growth and small dividends.