Medico Remedies Ltd (MRL) is a company that makes and sells medicines. It started in 1994 and mainly makes medicines for bacterial infections. The company also makes antibiotics, painkillers, diabetes medicines, heart medicines, antifungal and antimalarial drugs, anti-ulcer medicines, antacids, and vitamins. It also makes creams, gels, syrups, and other medicines for different health problems. The company has a factory in Palghar, where it produces 122.6 million tablets, 36 million capsules, and 0.12 metric tons of dry syrup every month. It uses good-quality ingredients from trusted suppliers to make safe and effective medicines. Harshit Mehta is the Managing Director of Medico Remedies Ltd. He studied pharmacy at the University of Mumbai and also studied family business management at S P Jain Institute in Mumbai. In the third quarter of 2024-2025, the company’s profit grew by 80.69% compared to the same time last year.

On May 26, 2022, the company moved from a smaller stock market (BSE SME) to a bigger one (BSE and NSE). In 2021, it gave extra shares to investors in a 3:1 ratio and increased its share capital from ₹4.5 crore to ₹17 crore. In 2023, it split one ₹10 share into five ₹2 shares. In 2022, 93% of the company’s money came from selling its own medicines, 3% from selling other goods, and the rest from labor charges, DEPB license transfers, and other income. The company sells its medicines in many countries, including the Dominican Republic (26%), Honduras (20%), Nigeria (12%), the Philippines (8%), Iraq (6%), Mali (6%), Myanmar (6%), and Kenya (4%).

India’s pharmaceutical industry was worth $42 billion in 2021 and may grow to $130 billion by 2030. India makes the most generic medicines in the world and supplies 60% of all vaccines. Many countries like the US, UK, Canada, and Europe buy medicines from India. In 2023, India’s domestic market was $41 billion, and exports made $25.3 billion. India has 670 US-approved medicine factories, the most outside the US. Major medicine hubs include Mumbai, Hyderabad, Bangalore, and Ahmedabad. The government helps medicine companies by giving money and tax benefits. In 2020, the PLI Scheme gave $2 billion to help Indian companies make better medicines. India is also making more of its own raw materials to depend less on China. Foreign companies can invest fully in new medicine businesses. India’s biotech industry is also growing fast. It made $1.8 billion in 2009-10 and is expected to grow more. With government support, new investments, and low-cost medicines, India’s pharma industry will keep growing.

Medico Remedies Ltd is a mid-sized pharmaceutical company in India. It makes generic medicines for pain, allergies, diabetes, and more. The company has a WHO-GMP approved factory, which means it follows high-quality standards. It mainly sells in India but also exports some products. Its market value is smaller than big pharma companies, but it is known for quality and affordable medicines.

Latest Stock News:

Medico Remedies Ltd’s stock fell by 19.99% to ₹50.7. It was the biggest loser in the BSE ‘B’ group. More shares were traded than usual. In the last month, the stock dropped 31%, and in the past year, it fell 42%. Even after this drop, the stock’s P/E ratio is 47.5x, which is higher than most Indian companies with a P/E below 25x. The company’s earnings are growing, so some investors expect good performance in the future. But if that doesn’t happen, investors may worry about the stock price.

Potentials:

Medico Remedies Ltd wants to grow by making good-quality, affordable medicines. The company plans to make more types of medicines for different health problems. It may increase production to make more medicines. It also wants to sell in more countries, which can help it earn more money. The company follows strict quality rules, so more people may trust its products. But there is a lot of competition, and its stock price goes up and down. If it manages money well and grows carefully, it can become a stronger company in the future.

Analyst Insights:

Market capitalisation: ₹ 469 Cr.

Current Price: ₹ 56.7

52-Week High/Low:₹ 90.0 / 34.8

P/E Ratio: 53.0

Dividend Yield:0.00 %

Return on Capital Employed (ROCE): 21.3 %

Return on Equity (ROE): 17.2 %

Medico Remedies has grown its profits well, but its sales growth is slow. The stock price is high compared to earnings and book value, making it expensive. Even though the company makes profits, it does not pay dividends. Promoters have reduced their stake, which may be a concern. Customers are taking longer to pay, affecting cash flow. There are also signs that the company might be adjusting interest costs to look better. It may be better to wait before investing until the stock price drops or the company shows stronger growth.

India is one of the biggest medicine makers in the world. It produces low-cost, high-quality medicines and vaccines used in many countries. India is the third-largest producer of medicines by volume and has been growing at 9.43% per year for the past nine years. India supplies 50% of the world’s vaccines, 40% of generic medicines in the US, and 25% of medicines in the UK. It has 3,000 drug companies and over 10,500 factories that make medicines. India also has the most factories approved by the US FDA outside the US.

India is called the “pharmacy of the world” because it supplies 80% of global HIV/AIDS medicines. The pharma industry is expected to be worth $65 billion by 2024 and $130 billion by 2030. The government wants the industry to reach $450 billion by 2047. India makes biotech products like vaccines, biosimilars, and new treatments. The biotech industry in India was worth $137 billion in 2022 and is expected to reach $300 billion by 2030. The medical devices sector, which includes hospital machines and equipment, is also growing. It is worth $11 billion now and is expected to grow to $50 billion by 2030.

India is a big exporter of medicines. It earns $50 billion from the pharma industry, with $25 billion coming from exports. About 20% of the world’s generic drug exports come from India. The pharma market grew by 5% in 2023 and is expected to grow by 9-11% in 2024. The pharma industry employs millions of people and is growing fast. With more research, better technology, and new investments, India will continue to provide affordable medicines to the world and remain a global leader in healthcare.

The government is making major improvements in healthcare, education, and taxation. Over the next three years, every district hospital will get a Day Care Cancer Centre, with 200 opening in 2025-26. Medical colleges will add 10,000 seats next year and 75,000 in five years. Research students in IITs and IISc will get better financial support through 10,000 fellowships. Medical tourism will expand with easier visa rules and private partnerships. INR 20,000 crore will support private-sector research, and more funds will go to the ‘Saksham Anganwadi and Poshan 2.0’ program for better nutrition. Foreign investment in insurance is now fully allowed, boosting the healthcare sector.

Taxes will become simpler with a new Income Tax Bill. Startups registered before March 2030 get three years of tax-free profits. Merging companies can use past losses for up to eight years. Tax return updates are now allowed for four years, with extra charges after two years. Tax collection (TCS) on goods sales will be removed, but tax deduction (TDS) on purchases will remain. The TCS limit for foreign remittances is now INR 10 lakh. Small charitable trusts get easier tax rules, and online tax appeals will continue.

These changes will improve healthcare access, support education, boost businesses, and simplify taxes.

Latest Stock News:

The Nifty Pharma index went up by 0.25% even though the overall market was weak, reaching 20,435.7. Some of the top-performing pharma stocks were Natco Pharma (up 2.52%), Glenmark Pharmaceuticals (up 1.95%), Laurus Labs (up 1.73%), Granules India (up 1.56%), and Dr. Reddy’s Laboratories (up 1.22%). On the other hand, some companies saw a drop in their stock prices, including J B Chemicals & Pharmaceuticals (down 1.8%), Mankind Pharma (down 1.36%), Gland Pharma (down 1.26%), Abbott India (down 0.48%), and Aurobindo Pharma (down 0.37%).

Potentials:

The pharma industry has a lot of room to grow because more people need healthcare, and the government is supporting it. More medical colleges are opening, new cancer treatment centers are being set up, and India is promoting itself as a medical tourism hub. Foreign companies can now invest more in insurance, which will also help healthcare grow. The government is also giving ₹20,000 crore to encourage research and new medical discoveries. Since India is a big supplier of medicines worldwide, companies have a chance to expand their business. Overall, the demand for medicines and healthcare services will keep increasing, making this industry a good place for future growth.

India’s pharmaceutical industry is growing fast. Right now, it is worth about $58 billion, but it is expected to double by 2030 and could reach up to $450 billion by 2047. This growth is happening because more people are dealing with health issues like diabetes and heart disease, the population is getting older, and there is a greater focus on overall health.

India also allows foreign companies to invest easily in the pharma sector, making it an attractive place for global investors. The country is the third-largest producer of medicines in the world and the biggest supplier of generic (low-cost) medicines, providing 20% of the world’s supply. With over 3,000 pharma companies and 10,000 factories, India is a major player in the global healthcare market.

The Nifty Pharma Index, which tracks the performance of India’s top 20 pharmaceutical companies listed on the NSE, closed at ₹20,390 on February 24, with a marginal gain of 0.02%.

Last 1 Year: Grew by 7.00% Last 5 Years: Grew by 20.8% per year on average Last 10 Years: Grew by 5.97% per year on average

The pharma sector has grown well in the long run due to rising demand for medicines, healthcare investments, and India’s strong position in generic drug production. However, stock prices are high, so investors should carefully choose where to invest.

Standard Glass Lining IPO is a book built issue of Rs 410.05 crores. The issue is a combination of fresh issue of 1.50 crore shares aggregating to Rs 210.00 crores and offer for sale of 1.43 crore shares aggregating to Rs 200.05 crores.

About Standard Glass Lining Technology Limited

Established in September 2012, Standard Glass Lining Technology Limited specializes in manufacturing engineering equipment for India’s pharmaceutical and chemical industries. With a fully integrated in-house production process, the company delivers end-to-end solutions tailored to its clients’ needs. Their consumers are from paint, biotechnology, pharmaceutical, and food beverages. Their promoters play a crucial role in the growth of the company as they are skilled and experts in leadership.

Its turnkey offerings encompass design, engineering, manufacturing, assembly, installation, and operational support for pharmaceutical and chemical manufacturing facilities.

The product range includes: Reaction Systems and Storage, Separation, and Drying Systems.

IPO Subscription Period

Open Date: January 6, 2025

Close Date: January 8, 2025

Allotment Date: January 9, 2024

Listing Date: January 13,2025

Stock Exchanges: BSE and NSE

Pricing Details

Price Band: ₹133 – ₹140 per Share

Face Value: ₹10 per Share

Minimum Lot Size: 107 shares

Investment Requirement:

Retail Investors: Minimum ₹14980 (107 shares)

Small Non-Institutional Investors (sNII): 14 lots (1498 shares) – ₹209720

Big Non-Institutional Investors (bNII): 67 lots (7169 shares) – ₹1003660

Credit of Shares to Demat: Friday, January 10, 2025

Listing Date: Monday, January 13, 2025

Cut-off time for UPI mandate confirmation: 5 PM on January 8, 2025

Book Running Lead Managers

Standard Glass Lining Technology Limited has appointed prominent financial institutions as book-running lead managers for the IPO:

IIFL Securities Ltd

Motilal Oswal Investment Advisors Ltd

Kfin Technologies Limited has been designated as the registrar for the IPO.

Promoter Information

Promoter: The promoters of the company are Nageswara Rao Kandula, Kandula Krishna Veni, Kandula Ramakrishna, Venkata Mohana Rao Katragadda, Kudaravalli Punna Rao and M/s S2 Engineering Services.

Shareholding:

Pre-Issue: 72.49%

Post-Issue: -

Financial Highlights

Revenue: In FY22 revenue was ₹241 crores, in FY23 it was ₹500 and in FY24 it is ₹549 crores.

Profit after Tax (PAT): FY22- ₹25 crore, FY23- ₹53 crores and FY24- ₹60 crores.

Net Worth: ₹448 crores

Total Borrowing: ₹174 crores

Key Performance Indicators (KPIs):

ROE: 20.7%

RoNW: 25.5%

P/BV: 5.7

EPS (Pre-IPO): ₹3.25

EPS (Post-IPO): ₹3.64

P/E Ratio (Pre-IPO): 43.04x

P/E Ratio (Post-IPO): 38.5x

IPO Objectives

The Company intends to utilize the Net Proceeds for the following purposes:

Financing capital expenditure requirements for purchasing machinery and equipment.

Repaying or prepaying, in full or part, certain outstanding borrowings of the Company, as well as supporting its wholly-owned subsidiary, S2 Engineering Industry Private Limited, in repaying or prepaying outstanding borrowings from banks and financial institutions.

Investing in S2 Engineering Industry Private Limited to meet its capital expenditure needs for purchasing machinery and equipment.

Supporting inorganic growth through strategic investments and/or acquisitions.

Covering general corporate purposes.

Subscription Status (As of January 07, 2025)

Retail: 19.97x

QIB: 1.81x

NII: 35.73x

Overall Subscription: 18.16x

Recommendation

We recommend investors to apply the IPO of Standard Glass Lining Technology Ltd, as the revenue is growing year on year and the demand of the industry has risen which is beneficial for the company. The grey market premium as of January 07, 2025, it is approximately 71% showing a great listing gain to investors. For long term the valuation post IPO are also reasonable compared to its peer companies like GMM Pfaudler Ltd, HLE Glasscoat Ltd, Thermax Ltd, etc. provides a better opportunity to investor in long term.

Divi’s Laboratories Ltd., a major global API (Active Pharmaceutical Ingredients) manufacturer, was founded in 1990 as Divis Research Center, focusing initially on Research & Development. Today, it stands as one of the largest API companies worldwide, specializing in Intermediates, Nutraceuticals, and custom synthesis for innovator pharmaceuticals. It has a significant export-oriented business, with a presence in over 100 countries, supplying around 160 diverse products. Divi’s Laboratories Ltd. has achieved significant milestones in its growth and operations. In 1995, the company established its first manufacturing unit in Choutuppal near Hyderabad. Over the years 1997-2001, it earned ISO-9002 and OHSAS-18001 certifications, underlining its commitment to quality and safety standards. By 2002, Divi’s expanded further with a second manufacturing facility at Chippada, Visakhapatnam, which later became an Export Oriented Unit (EOU), enhancing global reach.

In 2006-2008, the company developed Divi’s Pharma SEZ in Visakhapatnam for Nutraceutical production, expanding its custom synthesis and Nutraceutical portfolio to meet rising export demand. In 2011, Divi’s launched the DSN SEZ Unit at Visakhapatnam, increasing production capacity in generic and custom synthesis segments.

From 2014-2018, Divi’s Laboratories passed multiple international regulatory inspections, including from the US FDA and COFEPRIS (Mexico), establishing EIR status for Unit-II, Visakhapatnam, which addressed previous regulatory concerns. The company invested ₹1200 crore in 2019-2020 in brownfield projects, creating DC SEZ and DCV SEZ units that became fully operational in FY2021. These projects boosted Divi’s role in generic and big pharma markets. In 2023, Divi’s launched Unit-III in Kakinada, Andhra Pradesh, further expanding production capacity.

In line with its dedication to innovation and compliance, Divi’s has research centers in Hyderabad and at manufacturing sites, focusing on custom synthesis and process innovations. With two subsidiaries—Divi’s Laboratories (USA) Inc. and Divi’s Laboratories Europe AG in Switzerland—the company enhances its reach in Nutra product markets. Divi’s continued investments in R&D, global regulatory compliance, and strategic expansion reinforce its commitment to high-quality pharmaceutical solutions, positioning it as a prominent player in the global API market.

Financial Overview

Industry Outlook

The Indian pharmaceutical sector is experiencing both near-term challenges and long-term growth potential driven by strategic expansions, cost efficiency, and new market opportunities. Key factors impacting the sector include pricing pressures in generic products and logistics challenges due to disruptions like the Red Sea crisis, which has extended shipping times and increased costs. Many companies are proactively managing inventory and supply chains to mitigate these impacts, such as advancing shipments and diversifying supply sources.

In the generic business, pricing pressure remains a challenge, but there is healthy volume growth in base businesses. Companies are expanding their portfolio to address loss of exclusivity (LOE) for several drugs, projected for 2026, which opens opportunities to capture market share in high-value molecules. This trend aligns with the pharmaceutical sector’s increasing focus on specialty and complex products and API (Active Pharmaceutical Ingredient) markets, which are seeing robust demand.

Custom synthesis continues to drive growth, with rising demand from both new and existing customers. Many companies have expanded into contrast media manufacturing, particularly iodine- and gadolinium-based molecules, which present a growing opportunity in global diagnostic markets with an annual growth rate of around 10-15%.

The API sector is well-positioned for sustained growth as global companies look for reliable alternative suppliers due to changing procurement strategies. With recent capacity expansions across SEZ units in India, companies can leverage low input costs in areas like raw materials, freight, and power to enhance profit margins. As inflation moderates globally, Indian pharmaceutical companies may also benefit from cost rationalization strategies, improving their competitiveness.

Divi’s Laboratories and other Indian firms are positioned to capitalize on the long-term trend of increased API demand and are exploring new opportunities in contract media and GLP-1 products. As the global addressable market for contrast media grows (estimated at USD 4-6 billion), firms expanding in this space can anticipate sustained demand for innovative and cost-effective solutions. Meanwhile, backward integration and advanced R&D capabilities are key strategies, enabling companies to streamline production costs and strengthen market positions over the long term.

In summary, while near-term challenges like pricing pressure and logistics disruptions persist, the pharmaceutical sector’s shift toward specialty products, cost-efficiency, and expanded capacities paints a promising outlook for the long-term. Indian companies’ strategic investments in innovation, compliance, and operational efficiency will likely enable them to maintain double-digit revenue growth while meeting the increasing demands of the global pharmaceutical market.

Business Segments

Divi’s Laboratories has demonstrated strong segmental performance across several key areas, including generic APIs, custom synthesis, peptides, contrast media, and ongoing capacity expansions at strategic units. Each of these segments reflects the company’s focus on meeting growing demand while managing industry challenges such as pricing pressures and supply chain disruptions.

Generic APIs: Divi’s generic business has experienced healthy double-digit volume growth, although pricing pressure persists across the industry. Despite the pricing environment, Divi’s has expanded its market share in smaller API molecules, highlighting the company’s resilience and strategic positioning in the generic segment. Emerging generic products have also shown robust performance, underscoring Divi’s adaptability in a competitive space.

Custom Synthesis: There is a notable increase in demand for Divi’s custom synthesis services from both new and existing clients. The future pipeline for this segment appears strong, with a robust set of products advancing through various stages of development. Key contributions from this segment are expected to start from FY26, aligning with the company’s long-term growth vision.

Peptides: Divi’s Laboratories has placed significant emphasis on GLP-1 compounds within the peptide segment, focusing on solid-phase synthesis to meet customer-specific requirements. The company is also expanding capacities for these peptide products, especially for solid-based peptides used in GLP-1 fragments, a growing therapeutic area. This focus enhances Divi’s specialty offerings, enabling it to cater to high-demand, niche markets.

Contrast Media: The contrast media segment has delivered impressive results, with volume growth of 20-30% YoY. Divi’s engagement with major clients in this area is progressing, with various projects moving to advanced stages. The company is actively working on iodine-based molecules (some nearing commercialization) and gadolinium-based molecules (in qualification stages, with potential for commercialization by FY26/27). Increased RFPs (Request for Proposals) from customers in this segment underscore the growing demand for Divi’s contrast media products.

Kakinada Unit (Unit-III): Divi’s Greenfield expansion at Kakinada is progressing as planned, with Rs. 11.8 billion spent as of H1 FY25. Production is set to commence in December 2024 in a phased manner. This unit is part of Divi’s strategy to expand capacity for both regulatory and custom synthesis products, supporting future growth in demand.

Logistics and Supply Chain: Divi’s has been proactive in managing inventory and logistics challenges, particularly those arising from the Red Sea disruptions that increased transit times to 70 days. The company has addressed these challenges by advancing shipments by 3-4 weeks and maintaining higher safety stock to minimize supply interruptions.

Key Subsidiaries and Their Information

Divi’s Laboratories operates through two major subsidiaries, Divis Laboratories (USA) Inc. and Divi’s Laboratories Europe AG. These subsidiaries play a strategic role in the company’s global expansion and focus on specialized markets for pharmaceutical ingredients, particularly in custom synthesis and nutraceuticals.

Divis Laboratories (USA) Inc.: This subsidiary caters primarily to the North American market, focusing on the distribution and marketing of nutraceutical products and custom synthesis services. It helps Divi’s Laboratories establish a strong presence in the US, one of the largest pharmaceutical markets globally, and aligns with Divi’s mission to support local customer requirements while meeting stringent regulatory standards. It contributes significantly to the company’s nutraceutical portfolio growth and has enhanced relationships with major pharmaceutical clients by providing reliable supply chains and custom synthesis offerings tailored to local industry needs.

Divi’s Laboratories Europe AG (Switzerland): This subsidiary focuses on European markets, providing nutraceutical and pharmaceutical ingredients and supporting custom synthesis projects for clients in Europe. Divi’s Laboratories Europe AG serves as a critical hub for European operations and facilitates compliance with EU regulatory standards. It also strengthens Divi’s supply chain resilience by creating a local presence in Europe, enhancing service delivery and customer support. In FY25, Divi’s Laboratories Europe AG has seen robust demand in nutraceuticals, particularly for ingredients with high-quality standards essential for the European market. This subsidiary plays a key role in Divi’s market penetration in Europe, contributing to the company’s overall revenue growth.

These subsidiaries support Divi’s Laboratories’ strategic goals of expanding its global footprint and catering to diverse regional needs in the pharmaceutical and nutraceutical industries. They also provide a platform for Divi’s to directly engage with key markets, ensuring regulatory compliance, effective supply chains, and tailored customer support, aligning with the company’s vision of global operational excellence.

Q2 FY25 Highlights

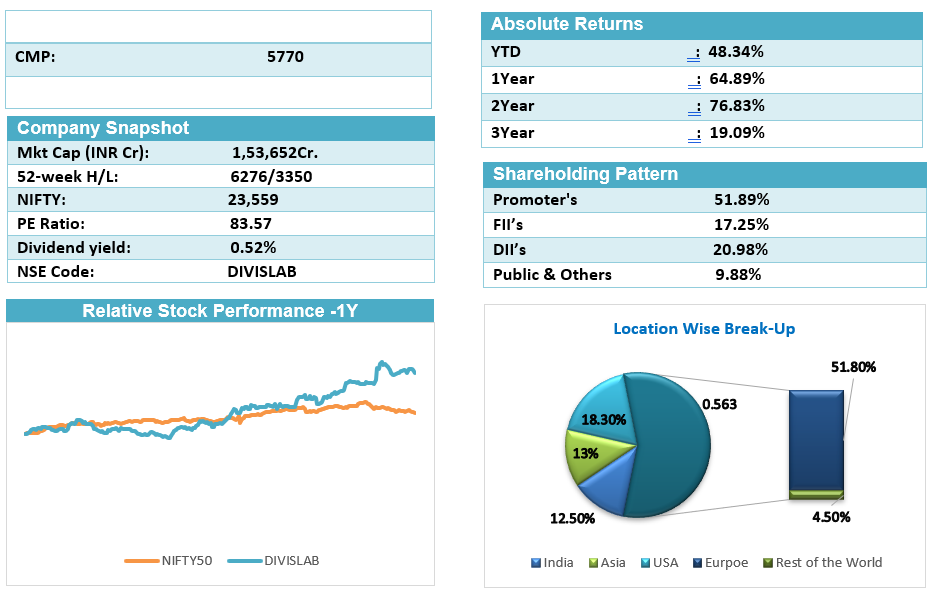

Divi’s Laboratories reported consolidated total income of ₹2,444 crore, a 22.5% increase compared to ₹1,995 crore in the same quarter of the previous year. For the half-year ended 30th September 2024, Divi’s Laboratories posted a consolidated total income of ₹4,640 crore, up by 20.4% from ₹3,854 crore in the same period of the previous year. This consistent revenue growth reflects the company’s ability to expand its product portfolio and global footprint.

Profit Before Tax (PBT) for the quarter was ₹722 crore, a substantial rise of 54% from ₹469 crore in the corresponding period last year. This increase in PBT highlights improved profitability driven by efficient operations and cost management. The PBT for the half-year was ₹1,326 crore, up from ₹961 crore, marking a 38% increase.

Profit After Tax (PAT) for the quarter stood at ₹510 crore, showing a significant 46.6% growth compared to ₹348 crore in the previous year. This reflects the company’s strong bottom-line performance, driven by both operational growth and improved cost efficiencies. PAT for the half-year was ₹940 crore, a significant 33.5% increase from ₹704 crore in the corresponding period of the previous year, reflecting robust operational performance and better margins.

The company also reported a foreign exchange (forex) gain of ₹29 crore for the quarter, which is a notable increase from the ₹1 crore gain recorded in the same quarter of the previous year. The company also recorded a forex gain of ₹28 crore for the half-year, compared to ₹14 crore in the previous year, further contributing to the positive financial results. The forex gain likely provided additional support to the bottom line.

Greenfield expansion at Kakinada Unit(III) is progressing as planned, with Rs. 11.8 billion spent as of H1 FY25. Production is set to commence in December 2024 in a phased manner. This unit is part of Divi’s strategy to expand capacity for both regulatory and custom synthesis products, supporting future growth in demand.

Divi’s has been proactive in managing inventory and logistics challenges, particularly those arising from the Red Sea disruptions that increased transit times to 70 days. The company has addressed these challenges by advancing shipments by 3-4 weeks and maintaining higher safety stock to minimize supply interruptions.

Financial Summary

INR in Cr.

Q2FY25

Q1FY25

Q2FY24

Q-o-Q (%)

Y-o-Y (%)

Revenue from Operation

2,338

2,118

1,909

10%

22%

Other Income

106

79

86

34%

23%

Total Income

2,444

2,197

1,995

11%

23%

Total Expenditure

1,622

1,496

1,430

8%

13%

Operating profit

716

622

479

15%

49%

Other Income

106

79

86

34%

23%

Interest

1

0

1

0%

0%

Depreciation

99

97

95

2%

4%

PBT

722

604

469

20%

54%

PAT

510

430

348

19%

47%

EPS (Rs.)

19.2

16.2

13.11

19%

46%

SWOT Analysis: Key Insights

Strengths

Market Leadership: Strong foothold in the industry with a leading market position.

Robust Manufacturing: Advanced manufacturing capabilities that ensure high-quality production.

Research Focus: Commitment to R&D fuels innovation and keeps the company competitive.

Outstanding Performance: Consistently strong financial and operational performance.

Weaknesses

Regulatory Risks: Exposure to regulatory changes can impact business operations.

High Dependency on API: Reliance on active pharmaceutical ingredients (API) poses risks.

Limited International Reach: Lack of significant presence in global markets limits growth potential.

Opportunities

Rising Global Demand: Increasing demand for pharmaceutical products worldwide.

New Product Development: Expanding product lines can capture new market segments.

Technological Innovations: Leveraging technology to enhance production and product quality.

Threats

Price Pressure: Competitive pricing in the market can impact profit margins.

Intense Competition: Facing stiff competition from both domestic and international players.

Supply Chain Vulnerabilities: Disruptions in the supply chain could affect operations.