Larsen & Toubro’s Growth: Investing in Defense and Advanced Technology for a Strong Future

Business and Industry Overview:

Larsen & Toubro Limited, abbreviated as L&T, is an Indian multinational conglomerate with interests in industrial technology, heavy industry, engineering, construction, manufacturing, power, information technology, defense, and financial services. It is headquartered in Mumbai, Maharashtra. L&T was founded in 1938 in Bombay by Danish engineers Henning Holck-Larsen and Søren Kristian Toubro. As of March 31, 2022, the L&T Group comprises 93 subsidiaries, 5 associate companies, 27 joint ventures, and 35 jointly held operations, operating across basic and heavy engineering, construction, real estate, manufacturing of capital goods, information technology, and financial services. It offers extensive IT services like application development, maintenance, and outsourcing; enterprise solutions; infrastructure management services; testing, digital solutions; and platform-based solutions to clients in diverse industries. It was a company that helped businesses with computers and technology. It started in 1996 and was part of a big Indian company called Larsen & Toubro (L&T). LTI helped banks, hospitals, factories, and insurance companies. It helped them store data safely. It used smart computers (AI) to solve problems. It kept information safe from hackers. It used machines to make work faster. It also helped businesses with cloud storage, websites, and mobile apps. LTI had offices in India, the US, Canada, Europe, and the Middle East. It worked with big companies in 30+ countries. Many Fortune 500 companies trusted LTI. It helped businesses move their work online. It kept their data safe. It helped them build better apps and websites. It made good money by helping businesses with technology. It grew fast because more businesses needed digital solutions.

Latest Stock News:

Larsen & Toubro (L&T) is making many new moves to grow its business. On April 4, 2025, L&T started a new company. This company is a fully owned step-down subsidiary. The company did not share full details, but this shows L&T wants to grow in new areas. On April 2, L&T also changed some top leaders in the company. This helps in bringing new ideas and better plans. On April 1, L&T got big new projects in its Power Transmission & Distribution business. This part of L&T builds electric lines and substations. These projects are from India and also from other countries. On March 26, L&T got its biggest project ever in its Offshore Hydrocarbon business. This part of the company works on oil and gas projects at sea. This shows L&T is trusted for big and complex work. L&T is also working on new technology. On March 25, its digital arm, Cloudfiniti, made deals with AI (artificial intelligence) startups. This means L&T wants to use smart technology in its work and offer better digital services. Even with all this good news, the L&T stock price went down a little on April 9, 2025. It closed at ₹3,126.05, which is 1.11% less than the day before. But the company is still strong. It has many projects and is working in both old and new areas. This can help the company grow more in the future. As of April 11, 2025, the Indian stock market went up because people felt more positive. This may also help L&T’s stock go up. The company is doing well with big orders and new plans in areas like power, oil, defense, and smart technology. L&T is also trusted for its strong work and experience. These things can help L&T grow more in the coming time.

Potentials:

Larsen & Toubro (L&T) has many big plans for the future. It will invest $12 billion in 5 years. Out of this, $4 billion will be for green hydrogen and green ammonia. It will build plants to make 2–3 million tonnes of these. It is buying 500–1,000 acres of land near the sea. It will also make electrolyzers. The first one will be used at Indian Oil’s Panipat plant. Later, L&T may work on fuel cells, big batteries, and hydrogen stations. In space, L&T is making India’s first private PSLV rocket with HAL. The rocket will launch in mid-2025. L&T also works with ISRO and helped in Chandrayaan-3. India’s space sector will grow to $44 billion, and L&T wants to grow in it. In defense, L&T wants to make more military items. It wants defense to be 10% of its business in 5 years. In real estate, it is building 28 million sq. ft. of new buildings. It will spend ₹7,000 crore to build an IT park in Vadodara, which will give 10,000 jobs in 5 years. L&T also started a chip company called LTSCT. It will build a $10 billion chip plant by 2027. It will make 15 types of chips. The Indian government will pay 90% of the plant cost. L&T wants to grow in clean energy, defense, space, chips, and buildings.

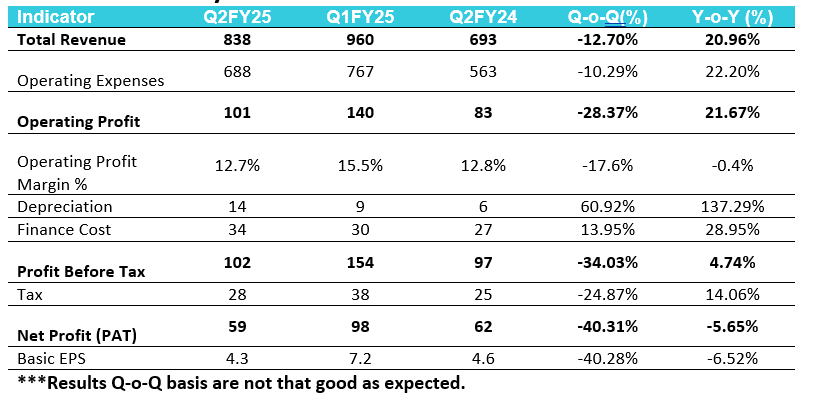

Analyst Insights:

- Market capitalisation: ₹ 4,28,537 Cr.

- Current Price: ₹ 3,116

- 52-Week High/Low: ₹ 3,964 / 2,965

- Stock P/E: 31.0

- Dividend Yield: 0.89%

- Return on Capital Employed (ROCE): 13.4%

- Return on Equity: 14.7%

Larsen & Toubro Ltd (L&T) is a strong and trusted company. It is growing well. Its revenue increased from ₹1.56 lakh crore in FY22 to ₹1.83 lakh crore in FY23, and then to ₹2.48 lakh crore in the last twelve months (TTM). This shows that the company is doing better every year. Its net profit also went up. It was ₹10,419 crore in FY22, ₹12,020 crore in FY23, and ₹16,531 crore in FY24 (TTM). This means the company is making more money. L&T has a return on equity (ROE) of 14.7%. This means it is using investors’ money in a good way. It also has a strong operating cash flow of ₹18,266 crore. This shows that the company has good cash in hand. L&T’s working capital days dropped from 55.8 in FY22 to 30.6 in FY24. This means it is managing its money, payments, and stock very well. The stock has a high price-to-earnings (PE) ratio of 31 and a price-to-book (P/B) ratio of 4.82. This is high, but fair because L&T is a leader in construction, defense, green energy, and other sectors. It also has many big orders in hand and is growing in India and other countries. This makes L&T a good company for long-term investment.