PB Fintech Limited: India’s Fintech Leader in Insurance and Lending—A Deep Dive

Business and Industry Overview:

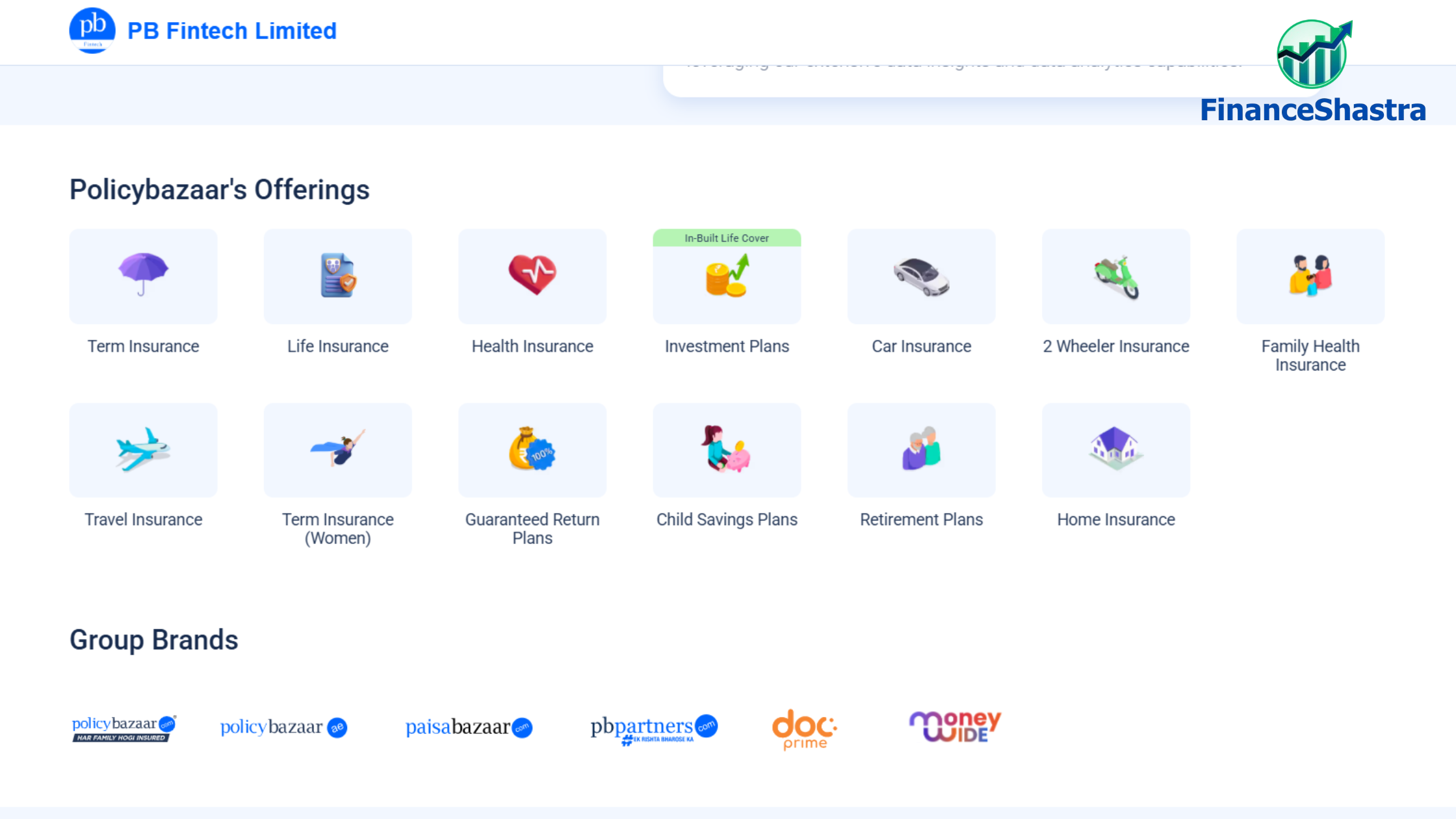

PB Fintech Limited is a leading Indian fintech company based in Gurgaon. It operates in two segments: insurance web aggregater/insurance broker services and other services. It has two main core platforms, Policybazaar and Paisabazaar, which offer digital insurance and lending products. It was founded in 2008 by Yashish Dahiya, Alok Bansal, and Avaneesh Nirjar. It was initially focused on insurance comparison but later expanded into direct insurance sales and digital lending. PolicyBazaar is India’s largest digital insurance marketplace (93% market share), providing health, term, motor, and travel insurance. As of Q2 FY25, it has 86.9M registered users and has sold 46.8M+ insurance policies. PaisaBazaar is India’s largest credit product comparison platform, serving 47 million+ consumers across 820+ cities and facilitating loans, credit cards, and credit score services. Apart from these two, they have PB Partners, a B2A2C (business-to-agent-to-consumer) platform enabling 250,000+ insurance agents through a Platform-as-a-Service (PaaS) model. The company operates under regulations from the Insurance Regulatory and Development Authority of India (IRDAI) and has expanded internationally to the UAE.

PB Fintech Limited operates an online platform for insurance and lending products in India. The company offers Policybazaar, an online platform to buy and sell insurance products, such as health, term, motor, and travel insurance products; savings and investment products; and B2B offerings for consumers and insurance partners. It also provides Paisabazaar, an independent digital lending platform that enables consumers to compare, choose, and apply for personal credit products, including personal, business, and home loans, as well as credit cards and loans against property. In addition, the company offers call centre and online healthcare-related services; online marketing, consulting, and support services; and support services in motor vehicle claims and related assistance, as well as engages in the online, offline, and direct marketing of insurance products.

Policybazaar.com has tie-ups with insurance companies that help it procure information such as prices, benefits, insurance cover, etc., directly from the insurers. Users can use the Policybazaar website or app to research, compare, and buy insurance policies from over 40 insurance providers. Policybazaar has companies that offer car insurance, health insurance, life insurance, corporate insurance, and travel insurance as its business partners.

The Insurance Regulatory and Development Authority of India regulates the insurance web aggregation business of Policybazaar. The company is registered as an insurance web aggregator under the Insurance Web Aggregator Regulations, 2017.

India secured the third position globally in fintech funding despite a 33% decline in YoY funding, which dropped to Rs. 16,475 crore (US$ 1.9 billion) in 2024, according to Tracxn’s Annual India Fintech Report. This reduction in funding reflects a broader slowdown in demand and ongoing geopolitical challenges. The fintech sector raised Rs. 24,279 crore (US$ 2.8 billion) in 2023 and Rs. 48,558 crore (US$ 5.6 billion) in 2022, underlining a significant decline over the past two years. Despite this, India remains one of the top three globally funded fintech ecosystems, only trailing the US and the UK.

With India moving towards a cashless economy and everything shifting to digital, there is a massive surge in the fintech industry in India, and PB Limited is one of the first companies to bring a platform that helps the customer to compare all the insurance policies available in the market and make a smart choice. It has 93.4% market share of online insurance sales in India.

Latest Stock News:

PB Fintech’s stock dropped 10% in two days, reaching an eight-month low of ₹1,322. It has fallen 41% from its January 2025 high of ₹2,246. The decline started after the company announced a ₹696 crore investment in its new healthcare subsidiary, PB Healthcare Services. Investors worry that such a big investment may reduce profits in the short term. The stock performed well in 2024, rising 165%, much higher than the Sensex (8%) and BSE Midcap (26%).

PB Fintech’s investment will give it a 33.63% stake in PB Healthcare on a fully diluted basis. Other investors, including senior executives, will also invest. This will bring the total investment to ₹828.75 crore, valuing the new subsidiary at ₹2,100 crore. The investment will be used to cover operational costs, improve branding, and drive strategic growth. The deal is a related-party transaction, which means a Registered Valuer will decide the valuation.

PB Fintech’s health insurance business is growing four times faster than the industry average. It is a major part of the company’s revenue. It contributes to over 60% of PB Fintech’s net present value (NPV) and makes up more than 30% of total premium collections. Despite the stock’s fall, some investors may see this as a buying opportunity because of the company’s strong growth in the health insurance sector.

Potentials:

PB Fintech has strong growth potential, driven by its improving financials, market leadership, and expanding presence in the digital insurance and lending sectors. With a ₹71.54 crore net profit in Q3FY24 and 48.31% YoY revenue growth, the company is on a positive trajectory. Policybazaar dominates the Indian online insurance aggregator space with 93% market share, while Paisabazaar leads in digital lending, giving PB Fintech a significant competitive edge. Additionally, its expansion into the UAE market with 2.4x YoY premium growth signals international growth opportunities. However, the company faces key risks, including regulatory scrutiny, highlighted by the recent GST raid, and increasing competition from fintech startups and traditional financial institutions. Disruptive technologies like AI, blockchain, and DeFi could reshape the industry, requiring PB Fintech to continuously adapt. Furthermore, like P2P lending platforms, the company must balance risk and return in digital lending, with potential stricter consumer protection laws affecting growth. Economic volatility, changing interest rates, and fluctuations in consumer credit demand could also impact performance. To sustain growth, PB Fintech must proactively navigate regulatory challenges, enhance risk management, and diversify revenue streams while staying ahead of technological disruptions. In Q2 FY25, the company introduced PaisaSave, a feature-rich co-branded credit card, and in Q3 FY25, it announced the beta launch of PB Money, a personal finance management tool built on the AA ecosystem.

Analyst Insights:

- Market capitalisation: ₹ 61,168 Cr.

- Current Price:₹ ₹ 1,332

- 52-Week High/Low: ₹ 2,255 / 1,090

- Stock P/E: 295

- Dividend Yield: 0.00 %

- Return on Capital Employed (ROCE): 1.75 %

- Return on Equity: 1.13 %

PB Fintech (Policybazaar) is a leading company in online insurance and credit services. It controls 93% of the digital insurance market in India. The company’s revenue has grown from ₹78 Cr in 2015 to ₹4,559 Cr now. This shows its strong brand, growing customer base, and good business model. It has 86.9 million registered users, which means many people trust and use its services.

The stock has given a 54.99% return in the last year, but in three years, it has fallen by 8.46%. This means the stock is volatile. Investors need to be careful before making long-term investments.

The company recently made a profit of ₹37 Cr after making losses earlier. However, its profit margins are still very low, at just 2%. Its return on equity (ROE) is only 1.13%, which is weak. The company has no debt, which is a good sign, as it does not have to pay interest on loans.

The stock is very expensive. It has a price-to-earnings (P/E) ratio of 295, which is much higher than that of other companies in the industry. This means investors expect very high growth, and if the company does not perform well, the stock price may fall. Its return on assets (ROA) is also low at 0.72%, meaning it is not making good profits from its total assets.

PB Fintech is a strong company with a good market position. It is growing fast but is not making enough profit yet. The stock is very expensive, making it risky. Investors should HOLD the stock and wait to see if profits improve before deciding to buy more.